Beyond the Grid: Global Infrastructure

We believe we are on the verge of making the grid great again.

Modern society runs on electricity, and the power grid is what keeps that power flowing across the economy. As electrification accelerates, the grid is becoming more important than ever, while pressure on existing networks continues to grow. In this article, we take a closer look at the challenges grid infrastructure faces today, how they could be addressed over time, and where we see the most actionable ideas as this transformation unfolds.

Table of Contents:

The Backbone of the Energy System

The Rising Demand for Electricity

The Aging Grid Infrastructure

The Need for Massive Investments

Governments Are Stepping In

A Grid of Actionable Ideas

Our Final Take on the Grid

For this thematic report, I collaborated with Aurelion Research, an independent research group focused on small- and mid-cap stocks and broader macro themes. Made up of former investment fund analysts, the team looks for value wherever it appears, from shipping and energy to growth technology.

1. The Backbone of the Energy System

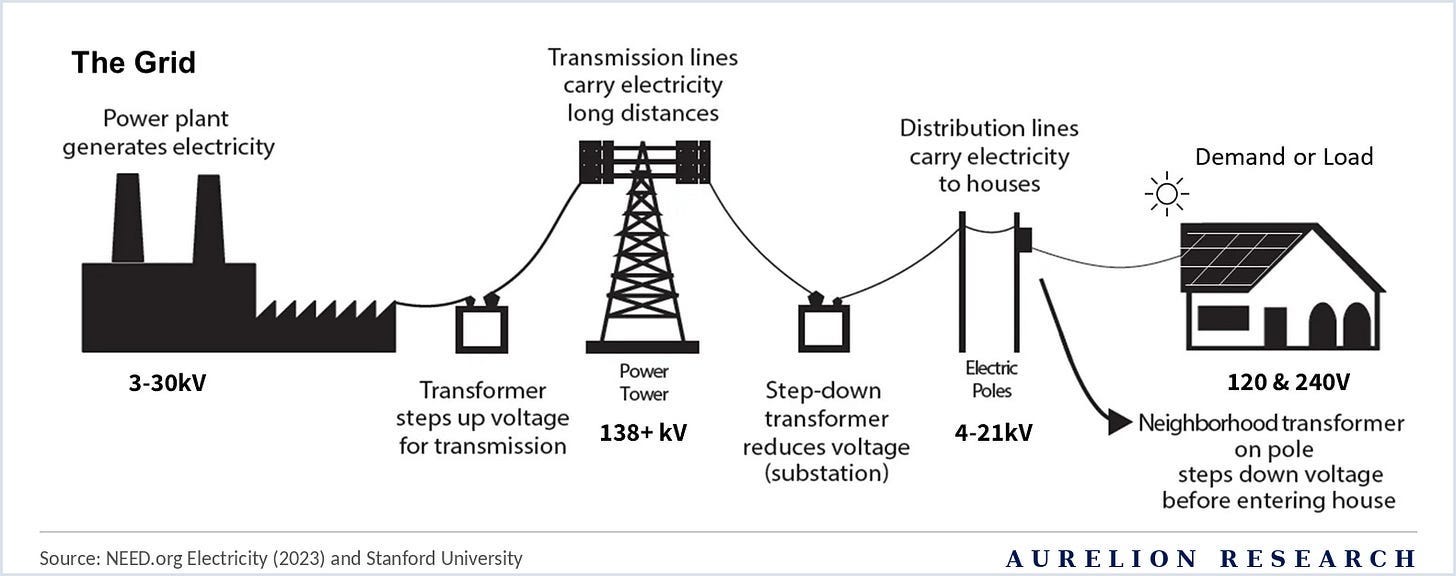

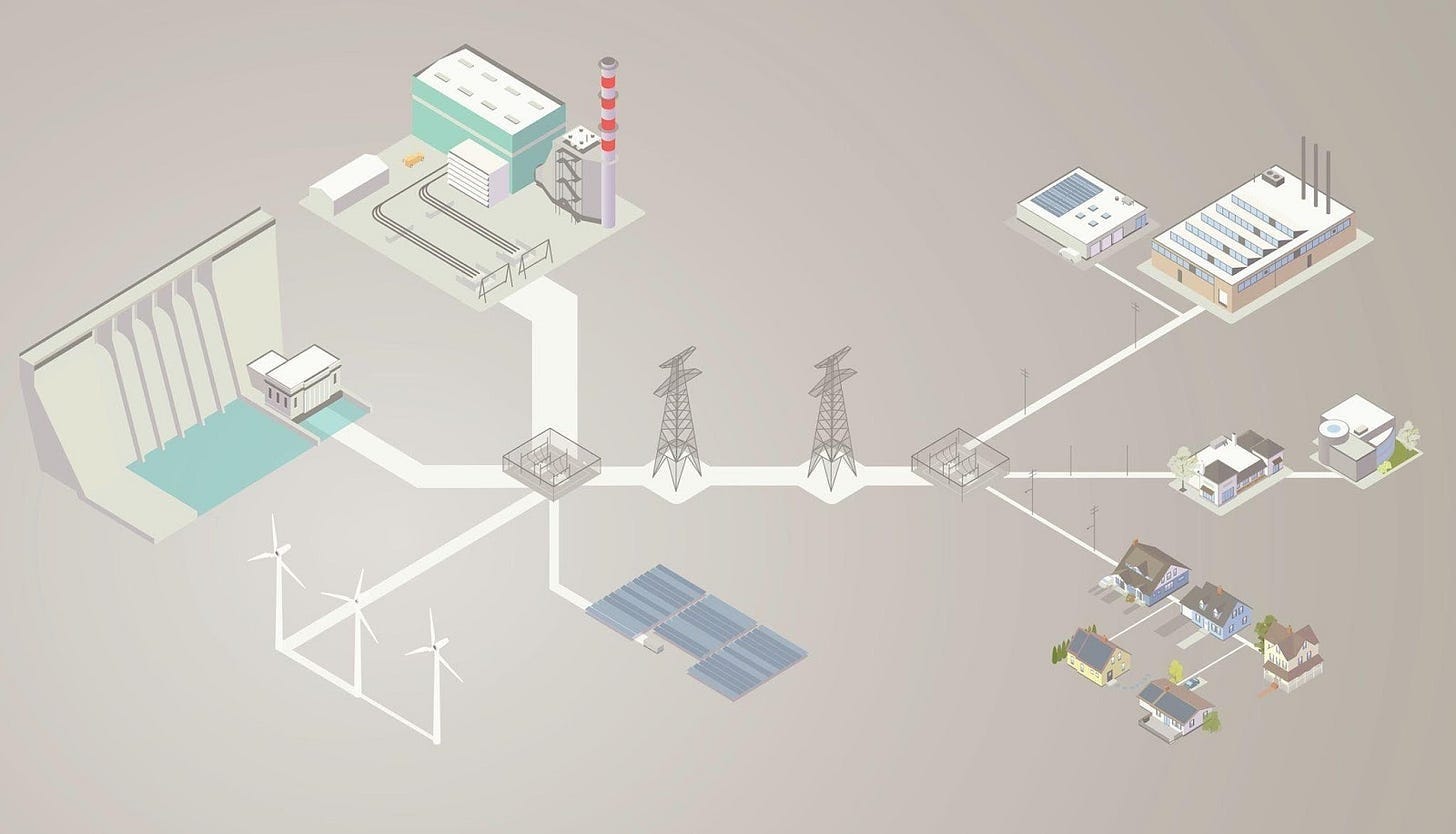

To start today’s thematic, a basic understanding of how the electricity grid is structured and how it works is essential. At its core, the grid is the infrastructure that connects electricity generation to end users.

Power plants generate electricity, which is then transported through high-voltage transmission networks. Closer to the point of use, that power moves through lower-voltage distribution networks, which deliver electricity to homes, factories, data centers, and the rest of the economy.

Although the core principle sounds simple, the system in practice is vast and highly complex. Electricity networks stretch across millions of km of power lines and rely on substations, transformers, digital control systems, and increasingly energy storage to keep power flowing smoothly across the grid.

All of these components have to work together in real time to ensure electricity is delivered the moment it is needed and that the broader system remains reliable and stable.

The Basic Architecture of the Power Grid

The exact structure of power grids varies widely across countries, shaped by geography, energy resources, and economic development. Even so, most power systems follow a broadly similar logic and face many of the same challenges. Those challenges are emerging on both sides of the system.

On one side, changes in how electricity is generated are reshaping power flows across the grid. On the other, shifting patterns of consumption are creating new demands on grid infrastructure. To understand where the most actionable ideas could emerge, we believe it is important to understand the challenges grids are likely to face in the years ahead.

1.1 Challenges for Power Grids

Power grids are entering a more demanding phase as the broader electricity system changes. Supply is becoming more dispersed, while consumption is rising and becoming more intensive. Much of the network in place today was built for a setup that was easier to manage, with steadier demand and more predictable flows.

That backdrop is changing quickly. New generation is being added across a wider set of locations, often beyond the parts of the network originally built to handle it at scale. At the same time, rising electricity use is creating heavier requirements in areas that need more capacity and flexibility. The result is a grid that is coming under increasing pressure.

A useful way to approach this is to separate the challenge into two parts.

One comes from changes on the generation side. The other comes from changes on the demand side. Together, they explain why grids are becoming harder to operate and why the need for investment is rising so quickly.

2. The Rising Demand for Electricity

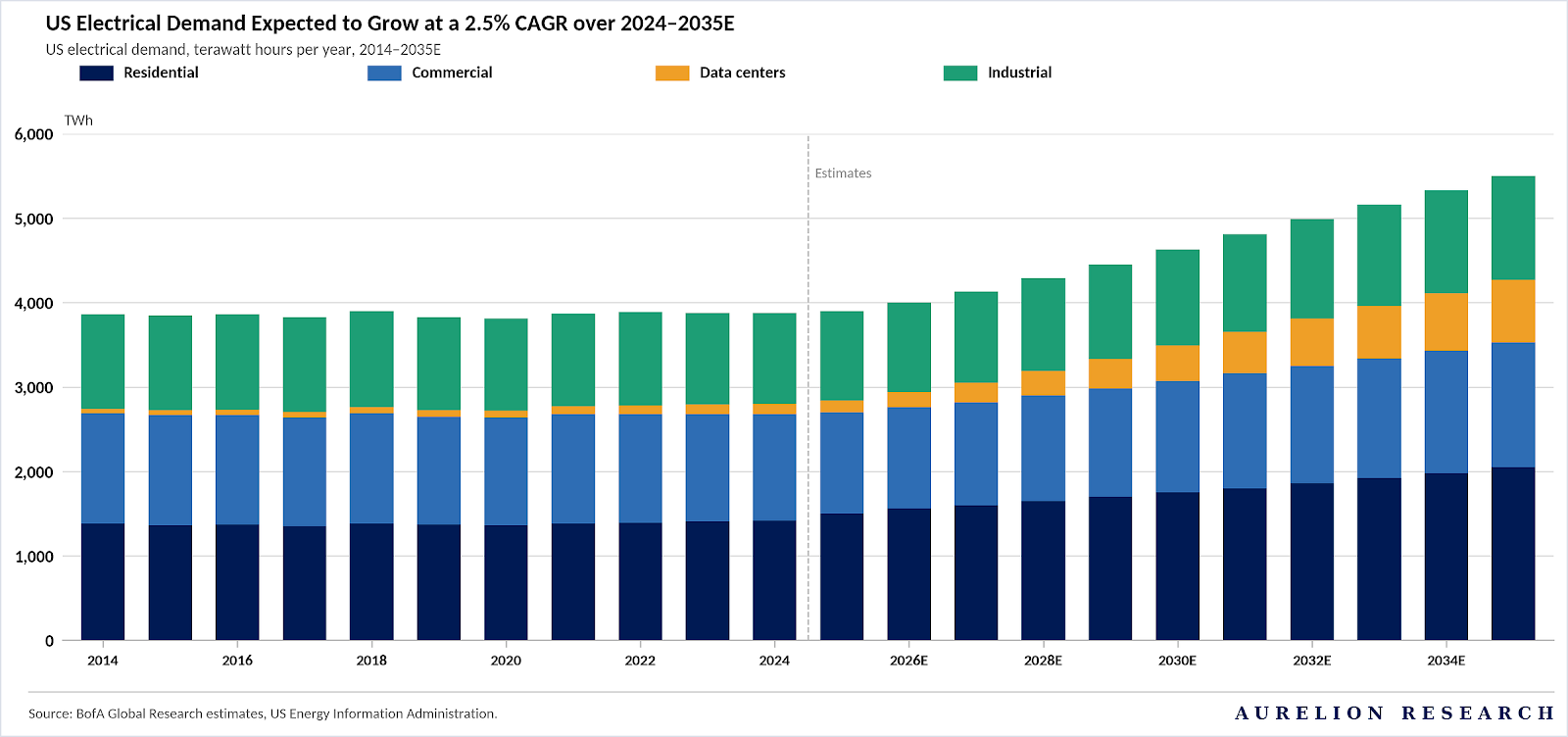

One of the clearest pressures on the grid comes from a simple reality: electricity demand keeps rising.

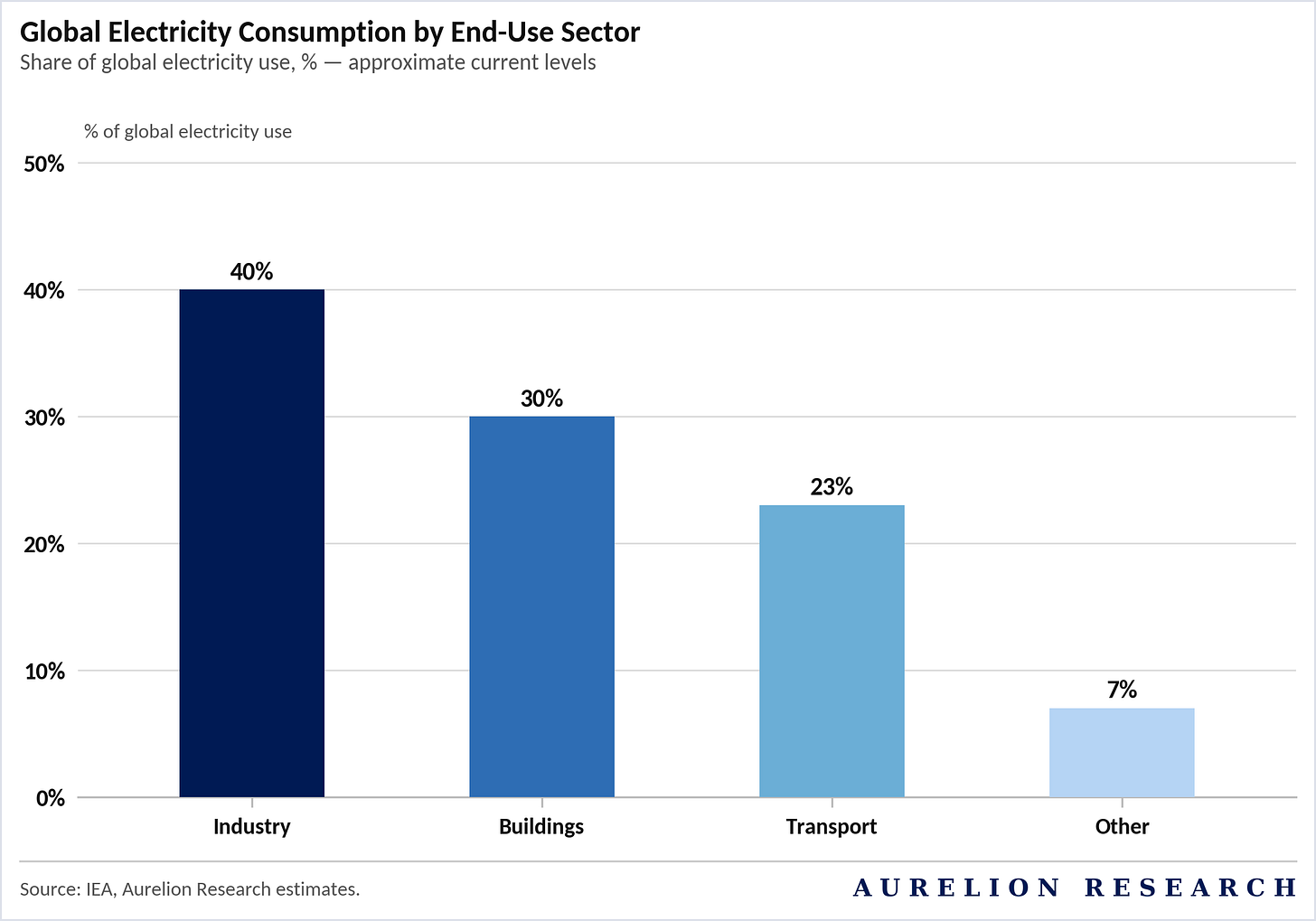

The chart below is a good place to start. Global power use is already enormous, and the demand base is broad. Industry remains the largest end market, buildings still account for a large share, and transport is becoming a more important source of load as electrification moves forward.

Part of that growth reflects the expansion of the global economy. As populations increase, incomes rise, and more countries continue to industrialize, electricity demand moves higher alongside them. Higher living standards bring more appliances, greater cooling needs, and a larger digital footprint, each of which adds to power use.

Industry is a major part of that picture. It already accounts for a large share of global electricity consumption and remains one of the most energy-intensive parts of the economy. As more industrial processes shift toward electrification to improve efficiency and reduce emissions, demand from this segment should continue to rise.

A similar shift is underway in buildings. Heating, cooling, cooking, and water heating are gradually moving toward electricity. That lifts underlying consumption and also changes when electricity is needed, especially during peak periods and seasonal swings.

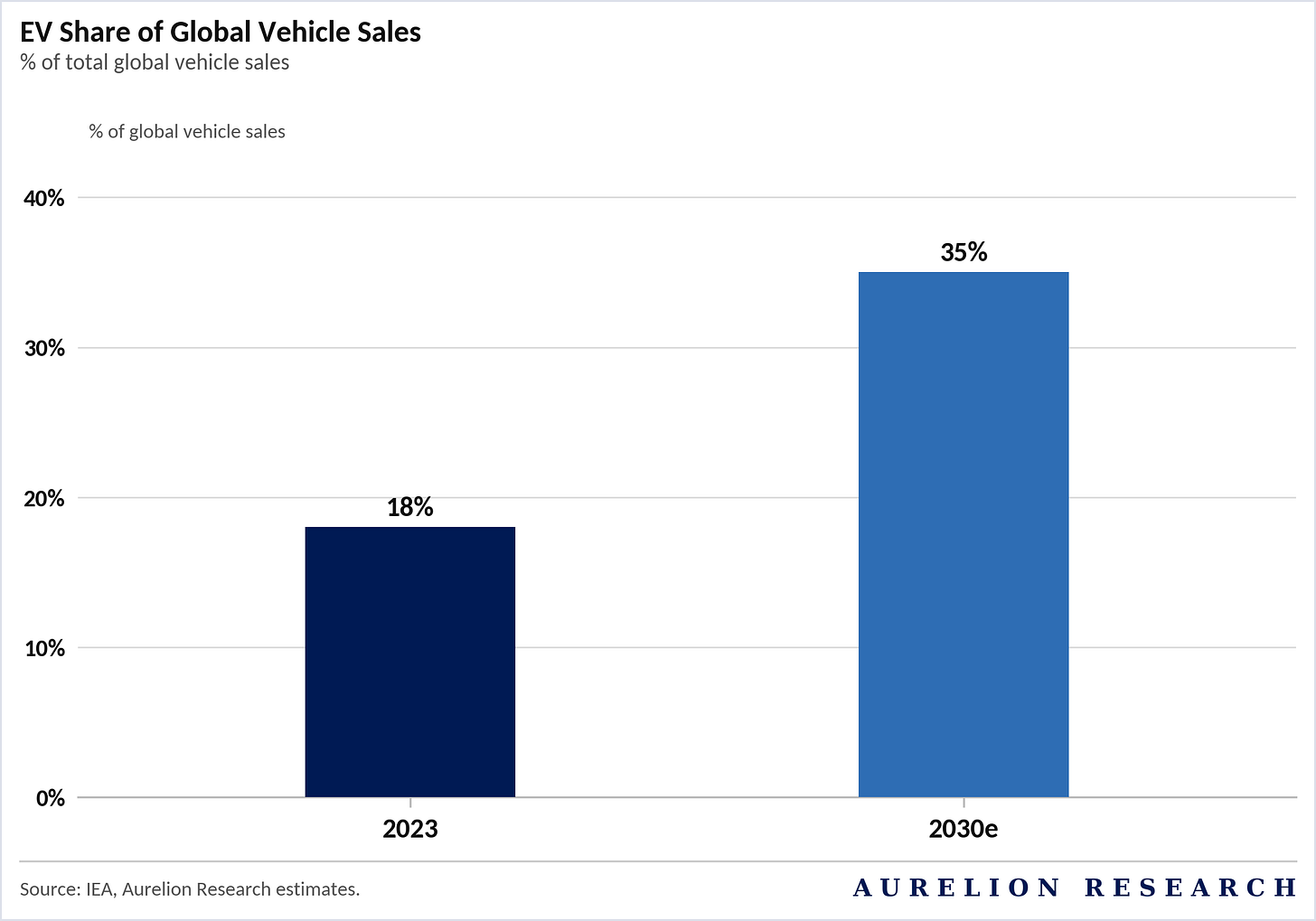

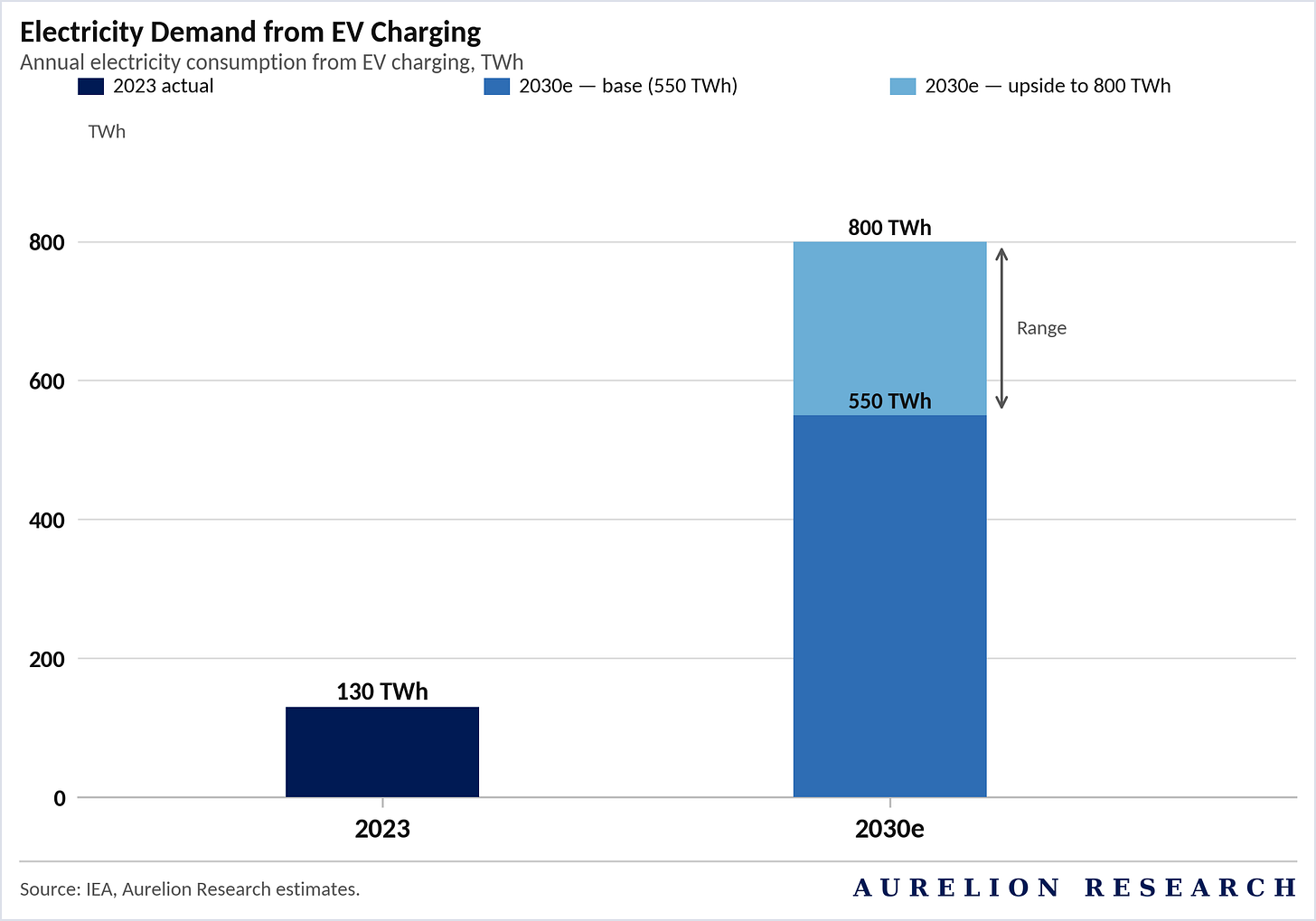

Transport adds another source of growth. Electric vehicles still represent a small share of the global fleet, but adoption is advancing quickly enough to create a meaningful new source of load for the power system.

That shift feeds directly into charging demand, which is expected to rise sharply over the rest of the decade. Pressure on local networks becomes more visible as that demand builds, especially in areas where charging demand rises faster than the grid was designed to handle.

Data centers are another fast-growing source of electricity demand. Their footprint is already meaningful, and expansion tied to cloud infrastructure and artificial intelligence is pushing it higher. These facilities can add very large, concentrated loads in specific locations, which makes the strain on the grid harder to manage.

That is why rising demand is such an important issue for power networks. Total electricity use is increasing, while demand patterns are shifting at the same time. Peaks are becoming sharper, and more of the new load is landing on distribution networks with greater local intensity. Existing infrastructure was built for a system with lower demand growth and a very different load profile. As electricity use rises across more parts of the economy, spare capacity begins to shrink. More parts of the network move closer to their limits, and the need for grid expansion becomes far more urgent.

3. The Aging Grid Infrastructure

While electricity demand keeps rising, large parts of the existing grid are already approaching the end of their operational lives.

This is especially visible in developed markets such as the United States.

According to industry data, around 31% of U.S. transmission lines and 46% of distribution lines have already exceeded their intended lifetimes or will do so within the next five years. That means a large share of current investment is going toward replacing aging infrastructure, not just adding new capacity.

This modernization goes well beyond replacing aging cables and transformers. It also includes upgrades to digital control systems, better monitoring capabilities, and new grid management tools that give operators more flexibility in balancing shifts in supply and demand.

3.1 The Growing Distance

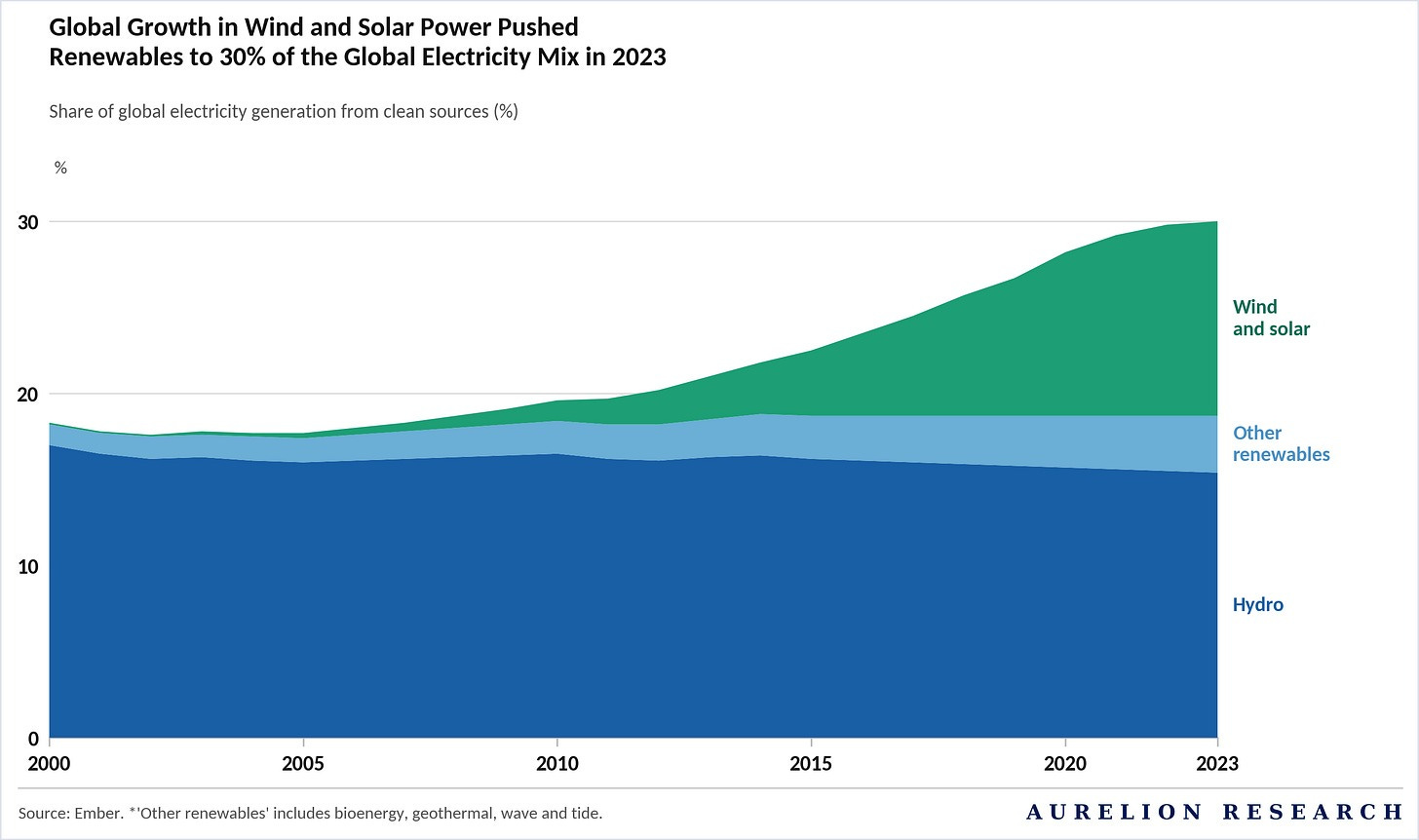

Now that we have covered the challenges on the demand side, it is time to shift focus to the generation side. Over the past few decades, renewable energy has taken a much larger share of global electricity generation. Renewables accounted for roughly 30% of global power generation in 2023, and that share is expected to keep rising in the years ahead.

Historically, electricity systems were built around large, centralized power plants located close to major centers of consumption such as industrial regions and large cities. As renewable energy takes a larger share of the mix, that pattern is changing. Wind parks and large solar farms are usually built where natural conditions are strongest, often far from the areas where electricity demand is concentrated. Solar projects are commonly located in high-irradiation regions, while wind capacity is frequently added in remote rural areas, along coastlines, or offshore.

That shift increases the distance between where electricity is generated and where it is consumed. As a result, transmission networks become more important because they must carry power across longer distances.

At the same time, generation is becoming more decentralized. Instead of relying on a limited number of large power plants, modern systems increasingly draw on many smaller generation sources spread across the grid. Some renewable capacity is also connected directly to local distribution networks, which adds another layer of complexity for those systems.

The implication is clear: electricity networks need to expand in order to connect generation that is increasingly located farther away from the areas where demand is concentrated.

3.2 The Timing Mismatch

Location is only one part of the challenge. Renewable energy also changes the timing of electricity generation. Traditional power plants can be ramped up or down to follow demand. Wind and solar depend on weather conditions, so output comes when the resource is available and not always when demand is highest. That creates a growing mismatch between electricity generation and consumption.

Energy storage can smooth part of that volatility, though it is unlikely to solve the issue fully, especially over longer periods. In practice, electricity often needs to be transported from regions with excess generation to regions where demand is stronger.

Grid management is evolving as well. In the past, system operators focused mainly on adjusting supply to meet demand. Today, they are also shifting electricity use toward periods when power is more available. That helps reduce congestion and improves the use of existing network capacity.

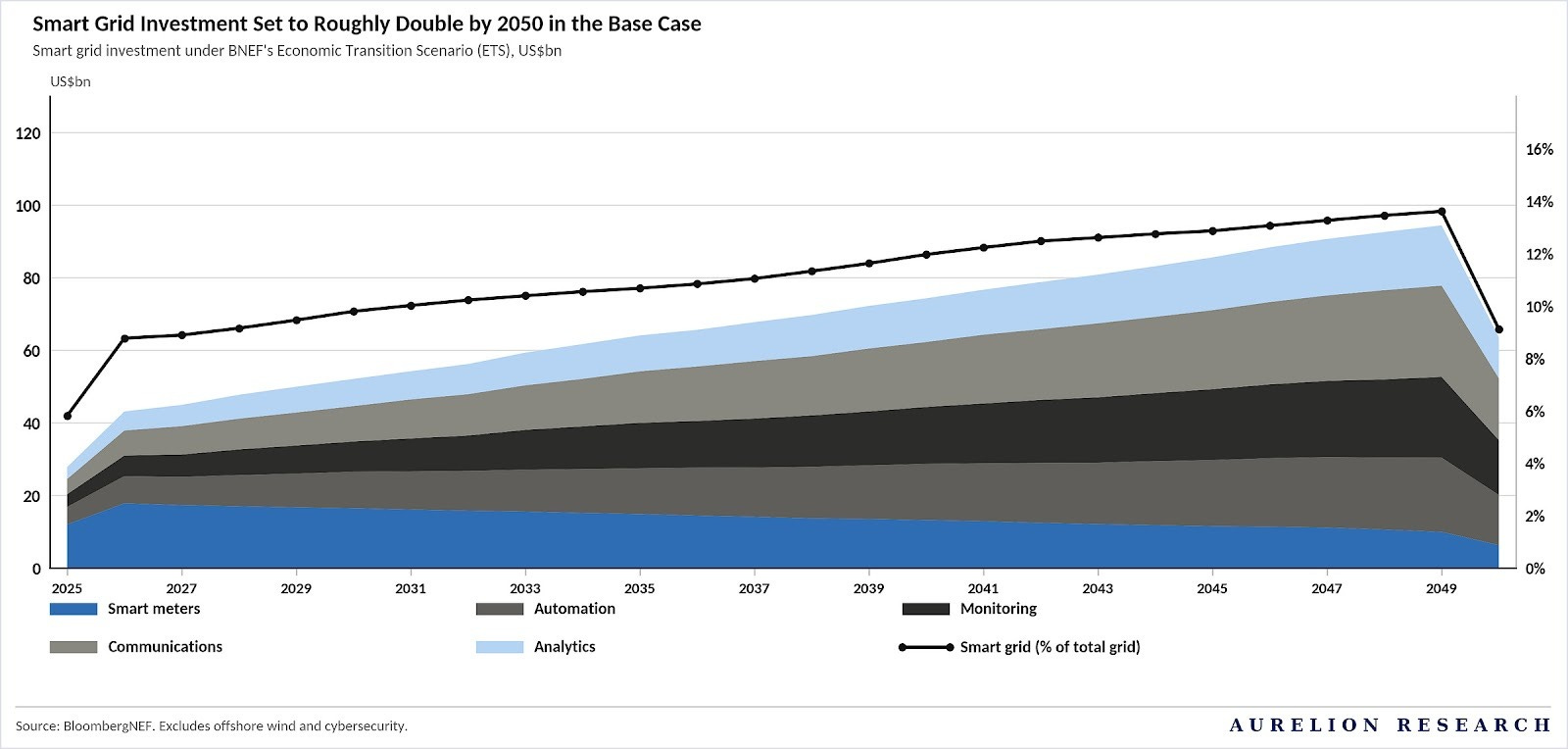

That shift is increasing the need for smart grids. These systems use digital tools to manage electricity flows more efficiently across the network. In turn, they improve flexibility, support system stability, and help the grid operate more effectively as generation and consumption become harder to balance.

4. The Need for Massive Investments

The grid is moving into a far heavier investment phase. The network in place today was built for a power system that was simpler, more centralized, and far less demanding than the one now taking shape.

Electricity demand is rising, generation is becoming more decentralized, and power flows are growing more complex. Existing infrastructure can no longer absorb that shift without significant expansion.

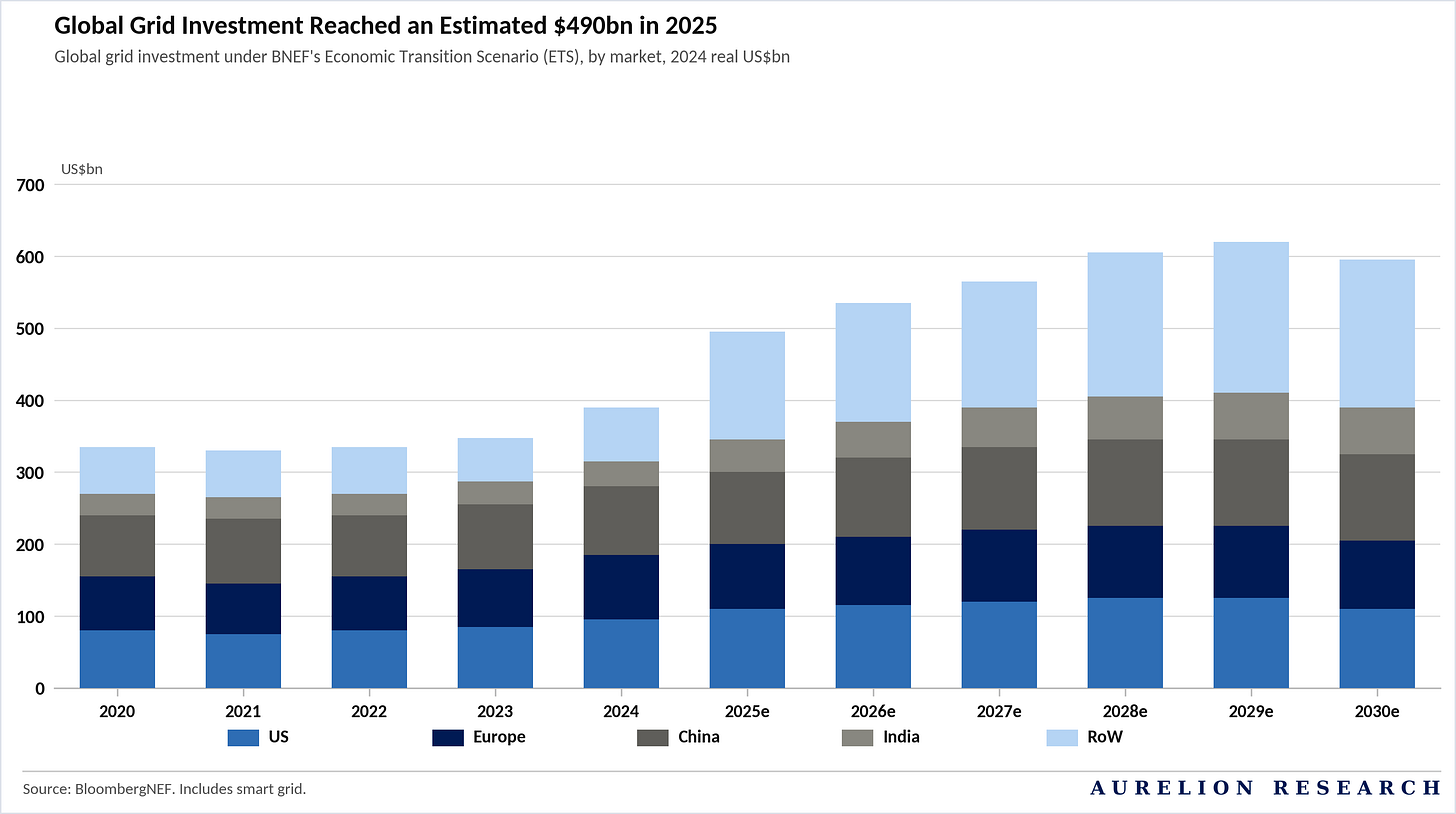

The spending outlook already reflects that shift. Global grid investment is estimated to have reached ~$490Bn in 2025, up from ~$390Bn in 2024, and BloombergNEF’s outlook points to spending approaching $600Bn by 2030. That goes well beyond routine upgrades. It points to a broader wave of capital deployment that is likely to extend through the rest of the decade.

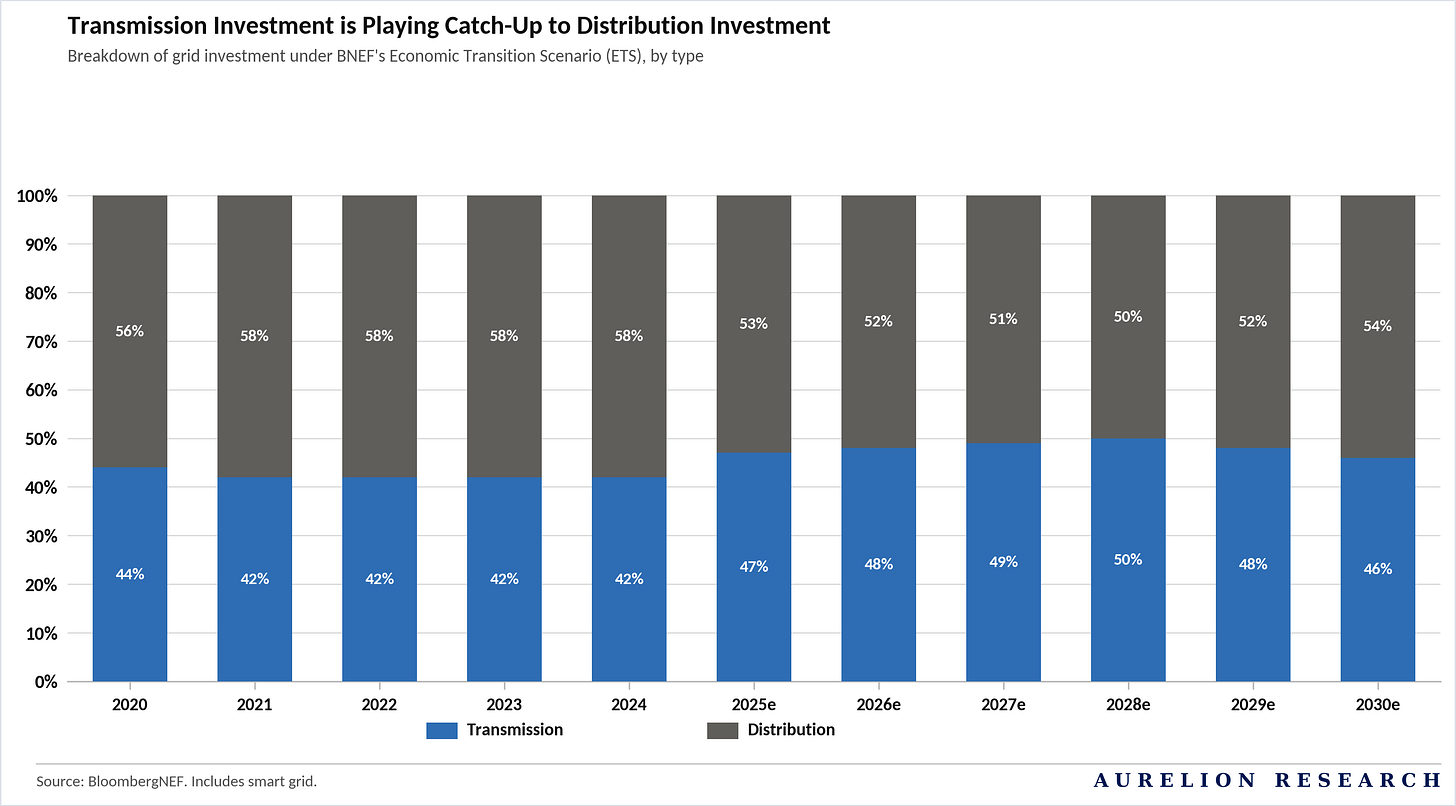

The mix of that spending is changing as well. Distribution still accounts for the larger share today, though transmission is gaining ground as utilities need more long-distance capacity to connect new sources of power and move electricity across wider areas. The data shows transmission rising from ~42% of total grid investment in 2024 to ~50% by 2028, before easing modestly to ~46% in 2030. Even so, the direction still points to a system that will require more backbone capacity alongside reinforcement at the local level.

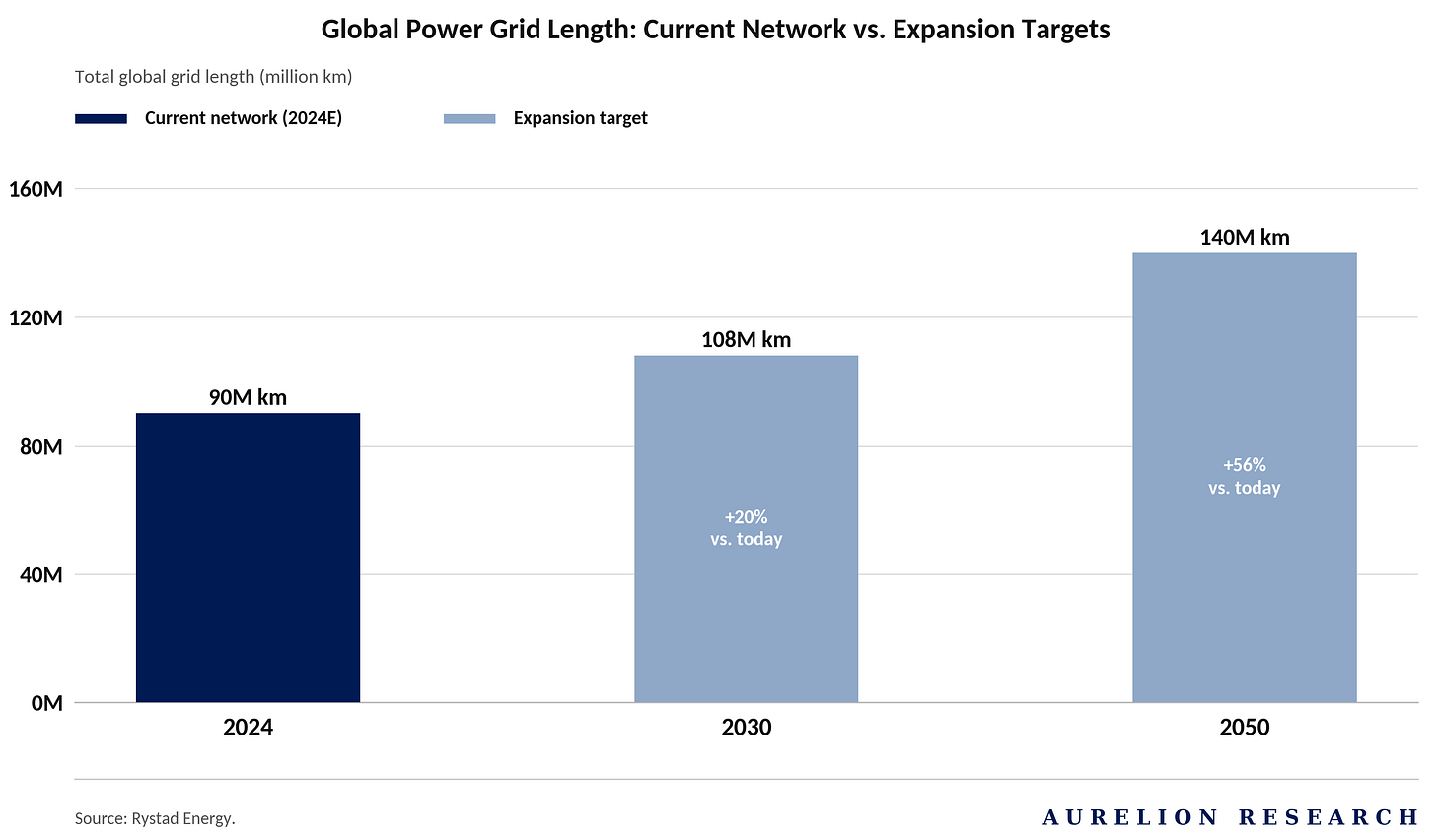

The scale of what lies ahead is just as significant. According to Rystad Energy, global power networks may need to expand by ~18M km by 2030 to keep pace with rising demand and the growing role of renewable energy.

That would represent an increase of about 20% from current levels. Looking further out, total global grid length could approach 140M km by 2050, which suggests the build-out still has a long runway ahead.

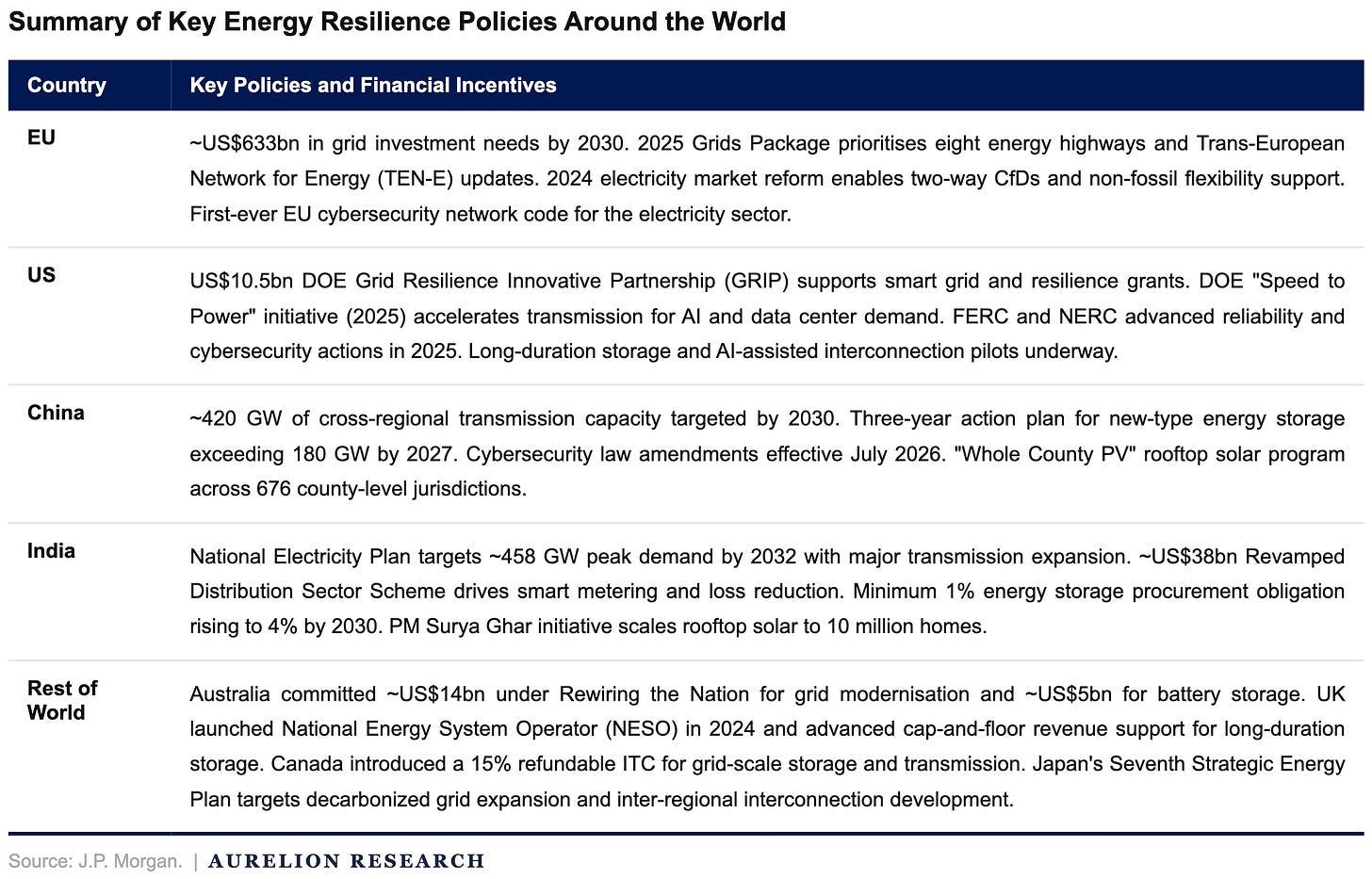

5. Governments Are Stepping In

Policy is playing a larger role in the grid build-out. Across many regions, governments are moving beyond broad decarbonization goals and taking a more active role in supporting the next phase of grid development.

We think that shift is important because grid expansion depends on more than capital. It also requires a policy framework that allows projects to move forward and earn acceptable returns.

The table below shows how different regions are responding.

As the table shows, the policy tools vary by country, but the broader direction is consistent. Grid modernization is receiving more support, resilience is becoming a bigger priority, and network investment is increasingly being treated as a central part of the energy transition.

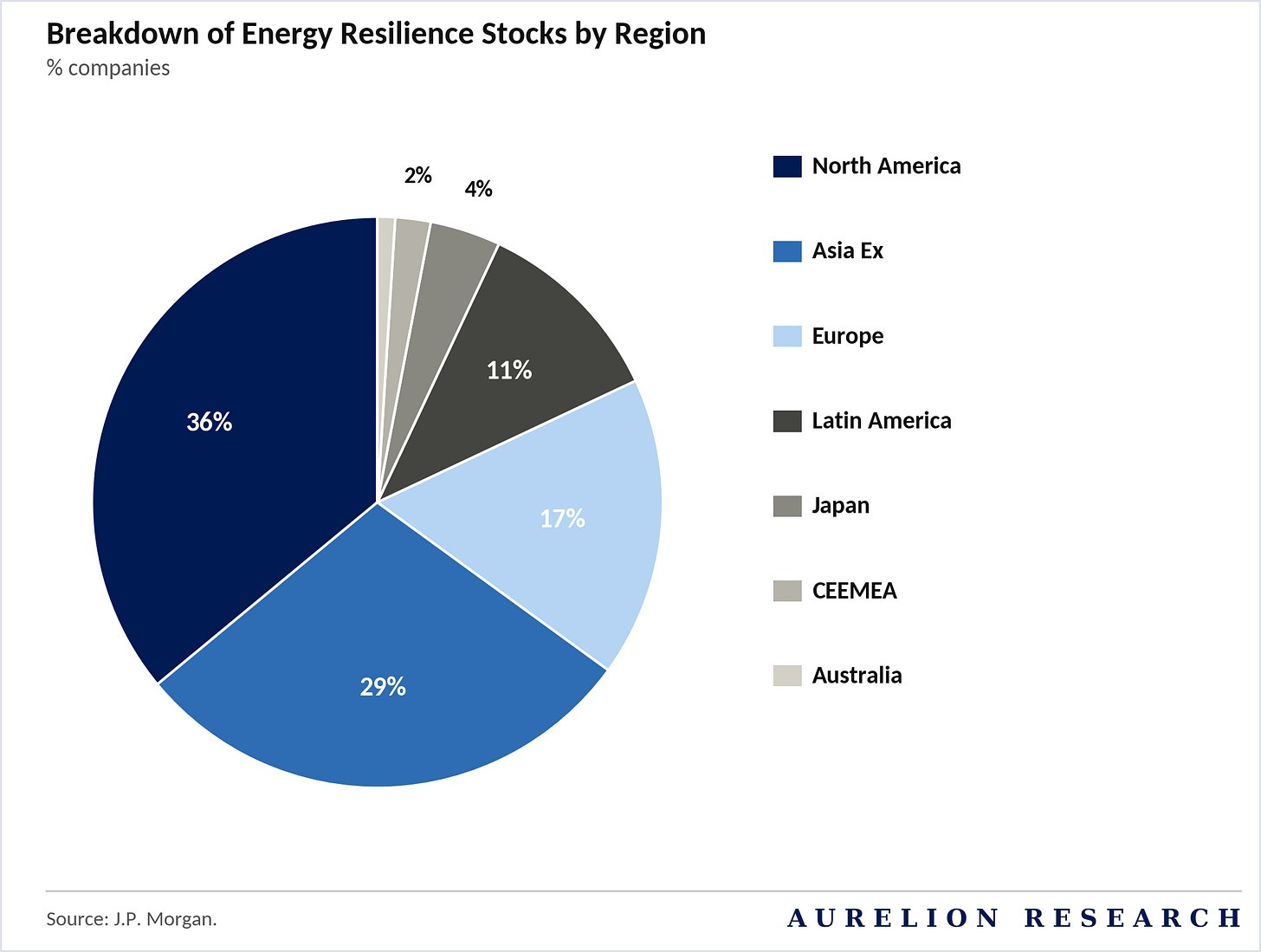

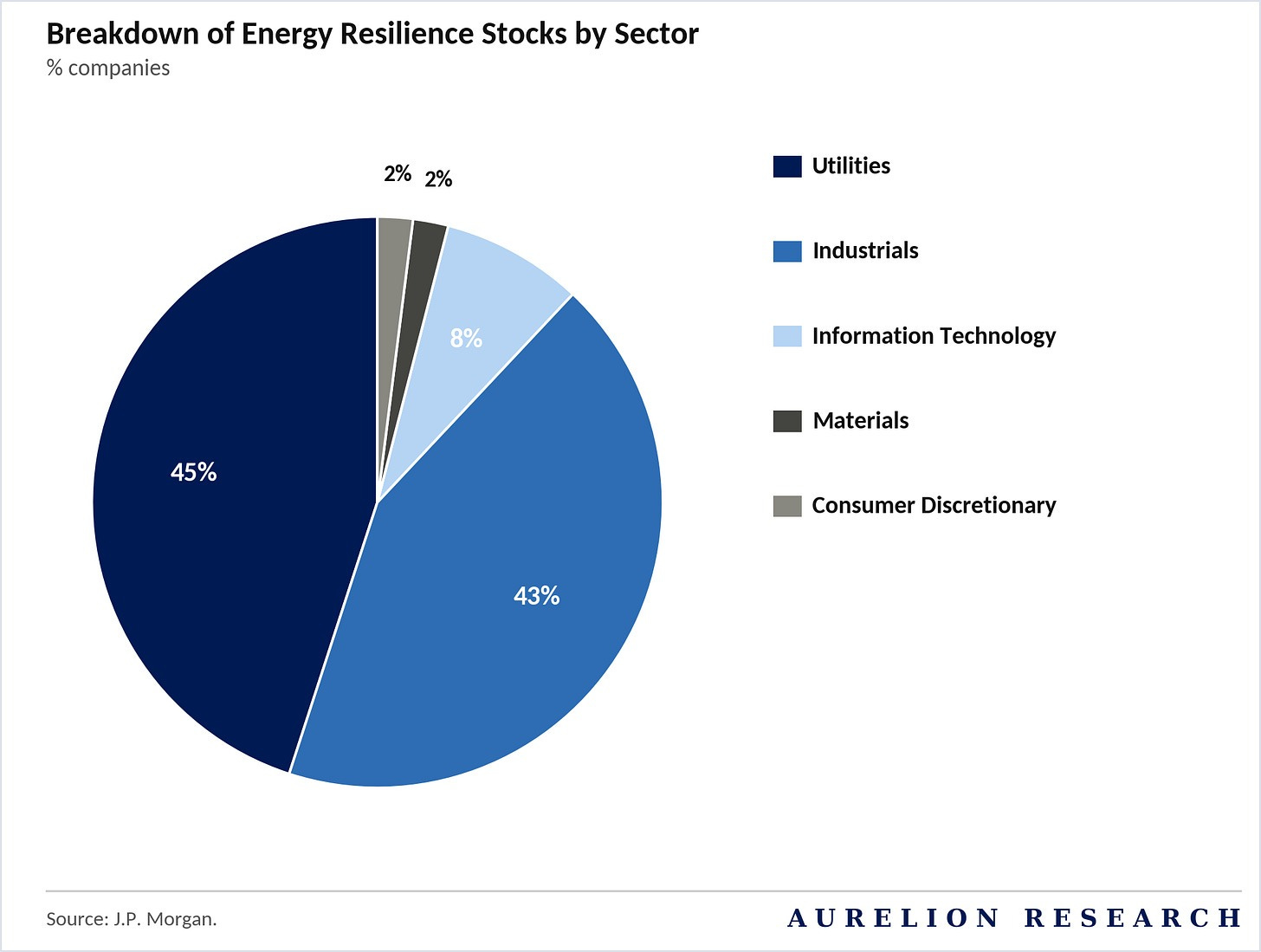

6. A Grid of Actionable Ideas

The grid build-out is a large and long-duration theme, though the investable universe is more concentrated than it may first appear.

The charts below show that listed exposure sits mainly in a limited number of regions and is weighted heavily toward utilities and industrials. That already helps frame the opportunity set. Exposure differs meaningfully across the market, and so does the quality of that exposure.

That is why stock selection carries so much weight here.

We believe the best ideas are the companies with the clearest link to grid investment, the strongest positioning, and the best ability to turn this cycle into durable growth and earnings upside. With that in mind, we now turn to the names we believe stand out most.

6.1 Bowman Consulting (BWMN):

A Cheap Small-Cap Name in the Grid Theme

Bowman deserves a place in this thematic because it offers something the larger grid names no longer do: meaningful exposure to the U.S. power infrastructure build-out at a valuation that still leaves room to move.

The company participates through engineering, design, and project support for power and utility infrastructure. Equipment manufacturers and large-scale contractors carry more balance sheet intensity and execution risk. Bowman’s model is lighter and sits further upstream, giving it a different return profile from the better-known names in the group.

That difference is part of the appeal. The stock carries rising exposure to transmission line design, substation engineering, utility undergrounding, and data center power infrastructure while trading at a clear discount to most E&C peers. Thematic relevance combined with valuation dislocation is what makes it worth including here alongside larger, better-followed names.

Bowman’s revenue base is expanding, and the power, utilities, and energy segment is taking a larger share of that growth. That shift changes how the market should value the business. A year ago, Bowman looked more like a broader engineering platform with some relevance to power. Today, the company has a stronger claim on the grid theme as utility undergrounding projects, gas pipeline work, renewables interconnection, and data center power supply contracts become a more meaningful part of the mix.

This exhibit shows that the business mix is improving. Total revenue rises from $346M in 2023 to $490M in 2025, with 2026 expected to reach about $564M. More important than the top line alone is the contribution from power, utilities, and energy, which grows from $64M in 2022 to an estimated $150M in 2026 and is on track to account for more than 25% of total revenue.

That shift gives Bowman more exposure to the parts of the market benefiting from grid hardening, utility capex, and rising power demand tied to AI infrastructure and electrification.

Utilities need engineering and design work before transmission lines are permitted, substations are built, or underground cable is installed. That puts Bowman earlier in the project cycle and gives the company exposure to the same capex wave driving the broader build-out.

For a smaller-cap name, that is an attractive place to be. Bowman can participate in what is shaping up to be a decade-long reinvestment cycle in U.S. power infrastructure, while carrying a lighter balance sheet and lower fixed costs than many peers.

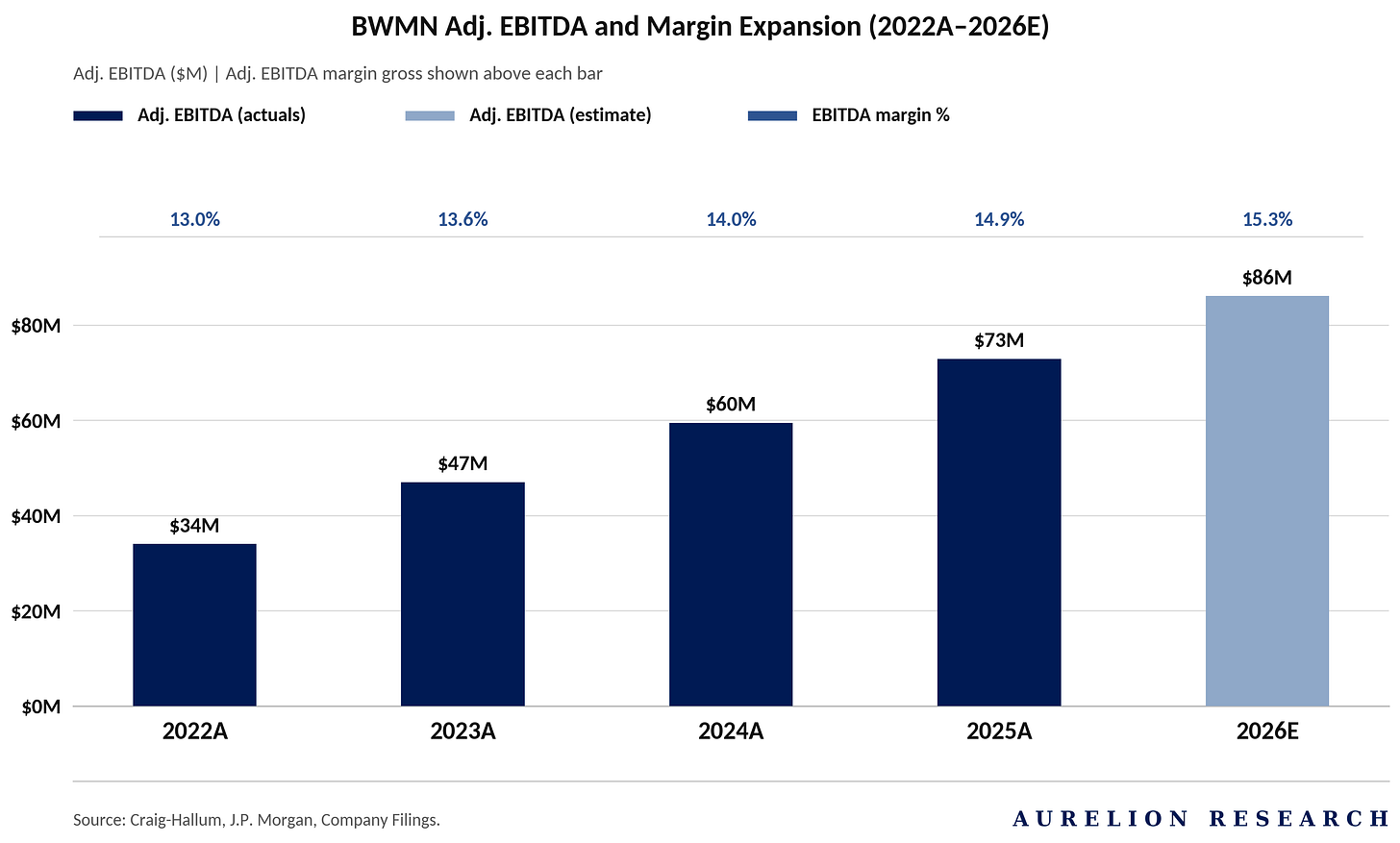

Margin expansion should follow naturally from that mix shift. As higher-value power and utility work becomes a larger share of revenue, the earnings profile should improve with it. BWMN has guided to 17.0% to 17.5% adjusted EBITDA margin for 2026, and Craig-Hallum views that range as conservative. That trend is already visible in the numbers.

BWMN Adjusted EBITDA has grown from $34M in 2022 to $73M in 2025, with 2026 estimates pointing to $86M. Margin has expanded steadily alongside that, from 13.0% in 2022 to 14.9% in 2025, with further improvement expected in 2026. That progression shows revenue growth is feeding into a stronger earnings profile as the mix shifts toward segments with better unit economics. Revenue growth draws attention first.

Margin expansion, as power and utility work takes a larger share, is what can push the stock higher once the market gives that shift more credit.

Backlog adds another layer. When a smaller company is tied to a large secular theme, the market needs proof that demand is already translating into booked work and not simply coming from a favorable macro backdrop. Bowman has that proof.

Backlog rose from $204M in 1Q23 to $479M by 4Q25, including 20% YoY growth at the latest quarter-end. Book-to-bill of 1.2x shows the pipeline is still growing. Power, utilities, and energy was one of the main drivers of order activity. For a company of Bowman’s size, a record backlog of nearly half a billion dollars gives strong support to near-term revenue visibility and shows demand remains solid.

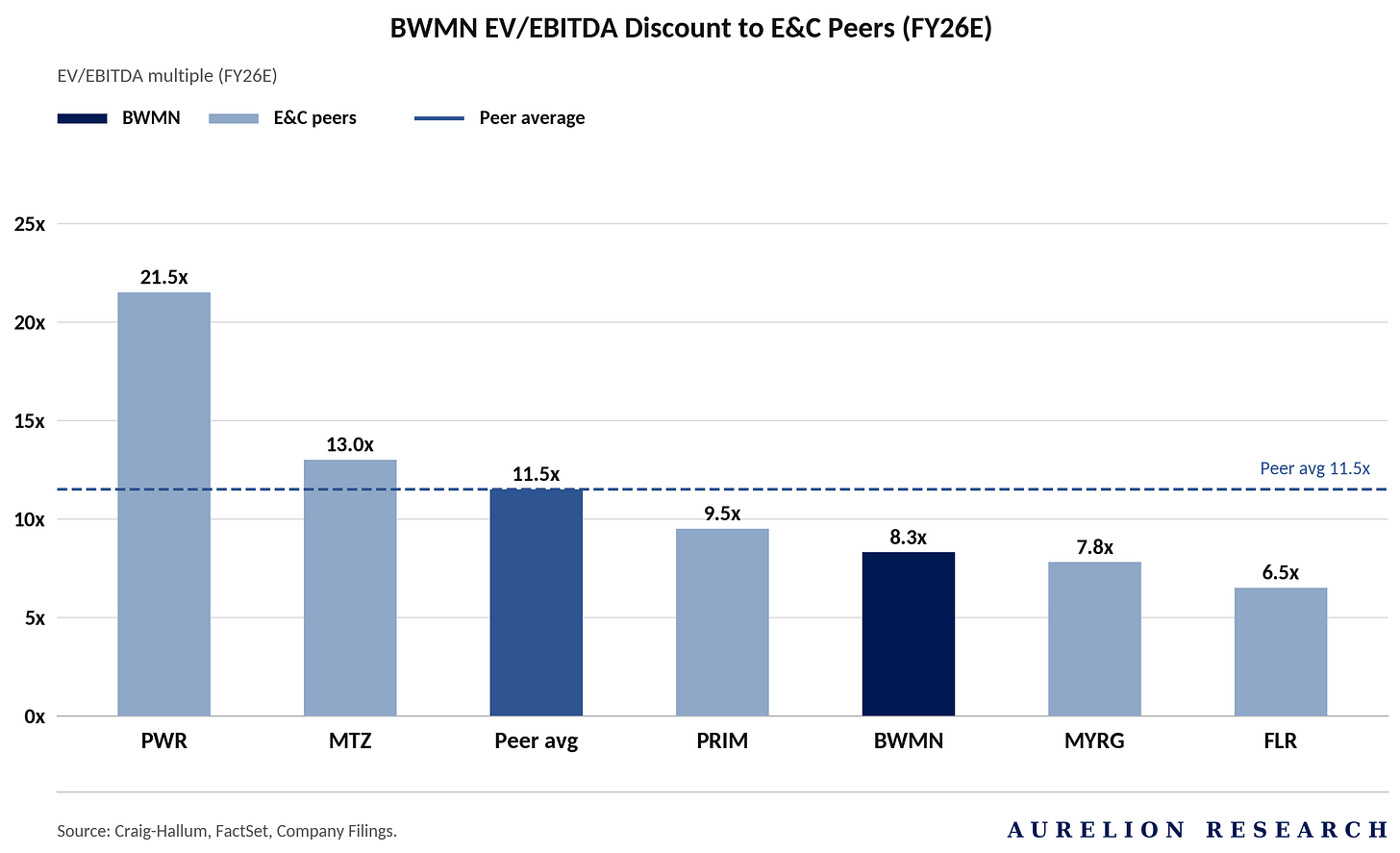

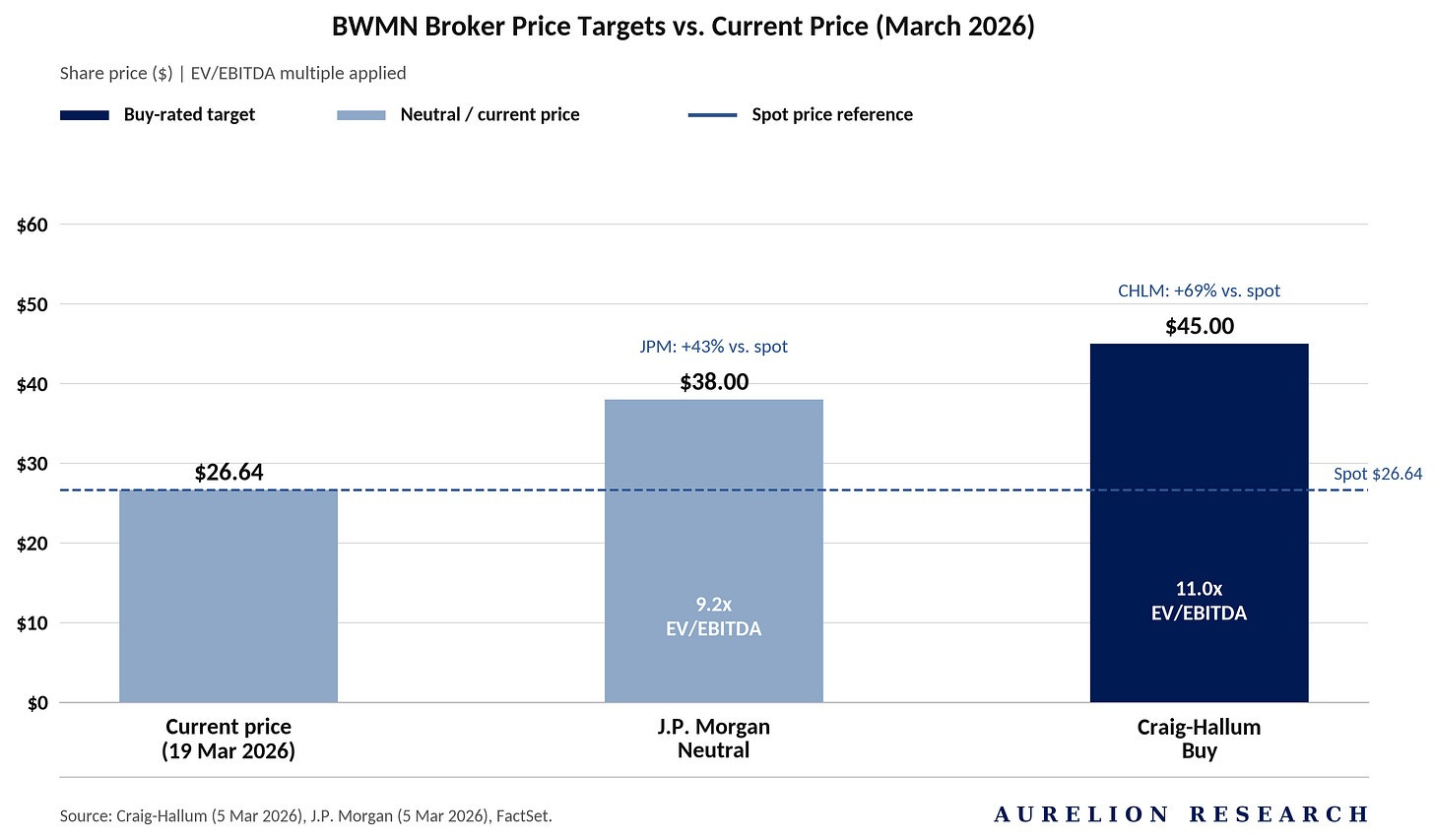

Valuation is where Bowman becomes especially compelling. The stock trades at a discount to the E&C peer group despite stronger growth, a record backlog, and a business mix that is becoming more relevant to the grid investment cycle with each passing quarter.

Bowman trades at ~8.3x FY26E EV/EBITDA against a peer average of ~11.5x, well below Quanta at over 20x and MasTec at 13x. That gap looks too wide given the company’s momentum and the direction of its end-market exposure. Bowman does not need to fully close it to generate a strong return.

Even partial convergence toward the peer group average would support meaningful upside from current levels, and the direction of the business argues for narrowing rather than a sustained discount.

The multiples behind those targets, 9.2x at J.P. Morgan and 11.0x at Craig-Hallum, look reasonable. They imply a valuation more in line with a growing engineering business that has strong backlog and clear exposure to the U.S. power grid build-out. Given the company’s recent momentum, that does not look demanding at all to us.

The story depends on execution. Bowman needs to keep converting backlog into revenue, integrating acquisitions including the December 2025 RPT Alliance deal which deepens its utility-scale power generation capability, and continuing to grow the power and utilities contribution. Progress on each front simultaneously supports earnings growth and multiple expansion.

We are bullish on Bowman. Power and utility revenue is growing, backlog has reached a record $479M, margins are improving, and the stock trades at roughly 8x forward EBITDA while peers trade closer to 11x to 21x.

6.2 Quanta Services (PWR):

A High-Quality Way to Play the Grid Build-Out

Quanta Services is one of the clearest ways to gain exposure to the grid build-out underway across NA. It sits close to the center of the spending wave moving through transmission, distribution, gas-fired generation, and data center-related power infrastructure. That opportunity is growing as the work becomes larger, more technical, and more difficult to execute.

That is where Quanta separates itself. Utilities and large customers increasingly need a contractor that can handle complexity across the full life of a project, from engineering and planning through installation and ongoing maintenance. Scale helps here. So does execution. Quanta has both. Its labor base, delivery record, and breadth of capabilities give it access to projects that many peers are less equipped to pursue.

The backdrop is favorable. Power demand is rising, the grid is aging, and the system needs a broad wave of investment to support higher load, new generation, and greater reliability. Data centers add to that need, but they are only part of the story. Grid hardening, interconnection work, and gas generation are also pushing spending higher. Quanta is positioned across each of those areas, which gives the growth case both depth and duration.

We are bullish on Quanta from here. Expectations into the March 31 Analyst Day still look reasonable relative to the scale of the opportunity ahead. The key issue now is less about whether demand is there and more about how far the current platform can carry the next leg of growth.

If management shows that the business can drive that growth without leaning too heavily on acquisitions, that should reinforce confidence in both the earnings path and the multiple.

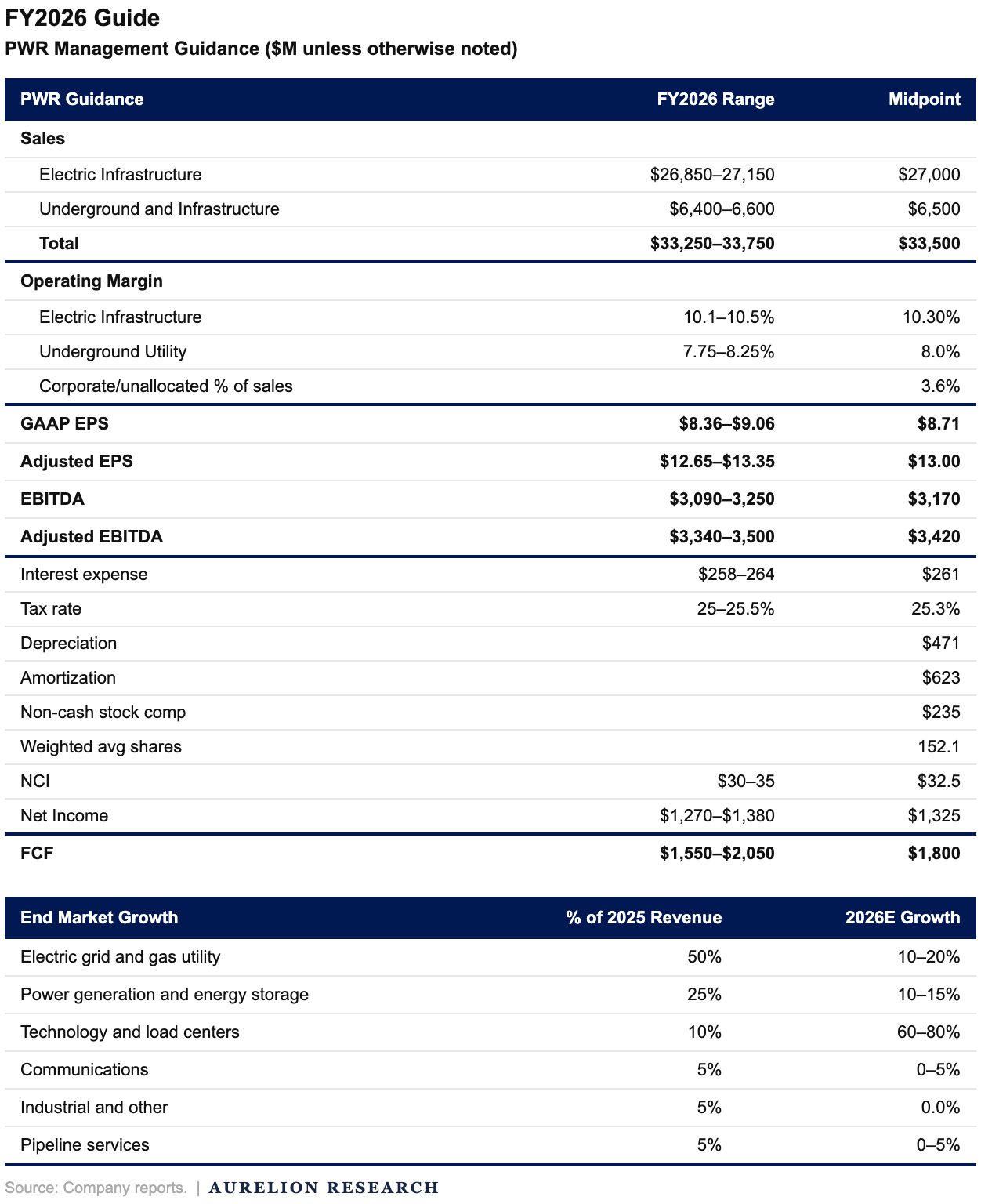

The guidance belongs here because it grounds the growth case in current numbers. The core utility business still provides visibility, while faster growth tied to technology and load center demand adds another leg of upside. That mix is attractive. It gives it a solid base of recurring infrastructure spend, with faster-growing categories adding incremental momentum on top.

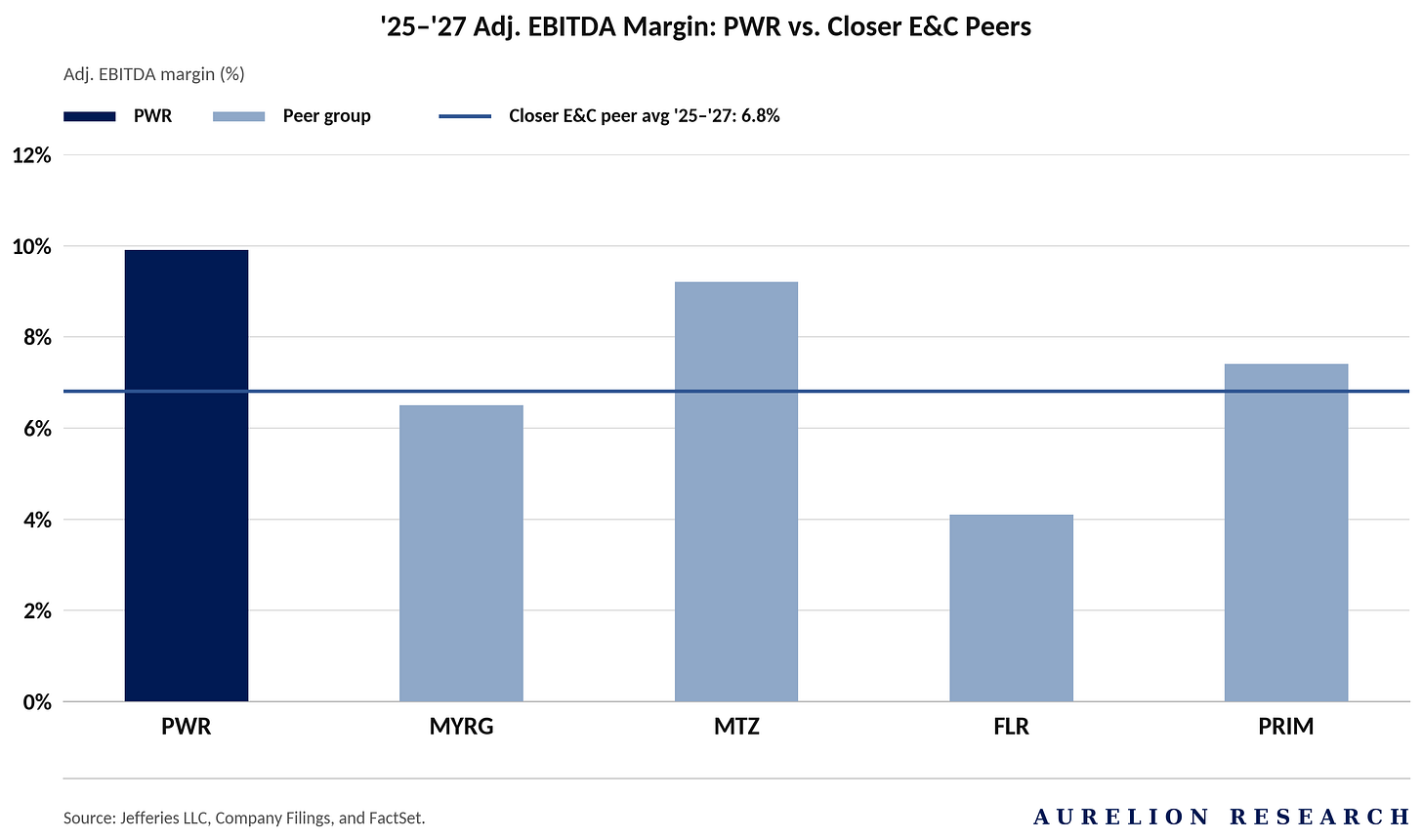

Profitability is another part of the case. Quanta already generates better margins than most closer E&C peers, and that gap says something important about the business. It points to a stronger mix, tighter execution, and a platform that has been able to convert favorable end markets into earnings more effectively than much of the group. A premium valuation still needs to be earned, but Quanta has given investors a solid reason to grant it one.

This exhibit fits best here because it supports the premium argument directly. Quanta is producing a higher margin profile than most peers, and that gives investors a concrete reason to treat the company differently from the rest of the group. The operating model adds to that edge.

Quanta self-performs more than 85% of its work, which gives it tighter control over project timing, quality, and execution. That also makes labor a competitive advantage. Skilled workers remain difficult to find across much of the market, and Quanta has more resources than most peers to recruit, train, and retain them. In a tighter labor environment, that edge can widen.

There are also shorter-cycle ways the story can improve. Many projects move through long development timelines, which means reported numbers can shift with permitting, procurement, right-of-way work, and customer readiness. That can create volatility from quarter to quarter, though it also creates room for upside when projects move faster and backlog converts earlier than expected. For PWR, pace of conversion is a major variable. Investors often focus on the size of the opportunity. The speed at which that opportunity turns into revenue and earnings is just as important.

That upside is visible in scenario work as well. We are aligned with Jefferies’ $765 upside case, which implies roughly 33% upside from a share price of $577. That framework assumes stronger revenue growth across both major business lines as Quanta attaches more deeply to data center-related demand and continues to win large power projects, with stronger margins creating upside to current numbers. It is an ambitious outcome, but still a reasonable one if execution stays strong and demand keeps building.

The balance sheet adds another layer to the thesis. PWR has already shown that it can allocate capital productively across acquisitions and repurchases, and that flexibility should stay valuable over the next several years.

In a market growing quickly, financial capacity gives management more ways to extend capabilities, widen its lead, and support earnings growth.

Valuation still deserves discipline. At ~31x 2028 earnings, Quanta is not cheap, even after accounting for the quality of the business and the strength of the end markets. The premium holds only if it keeps converting backlog, executing well on large projects, and protecting margins as it scales. That is a high bar. Quanta has cleared similar bars before, which is why the stock continues to command a premium inside a group that has already re-rated.

There are still risks worth keeping in mind. Warranty exposure is one. Large project work often carries long-dated obligations, and acquired portfolios can bring legacy exposure. Timing is another. Work under master service agreements is not always awarded evenly, and customer approvals, safety rules, and regulatory processes can all influence when revenue begins and how efficiently projects move. But even with those risks, we believe Quanta stands out as one of the strongest ideas in the space. The stock already reflects part of that quality, so the path higher will continue to depend on delivery. Still, with power infrastructure spending set to remain strong for years, Quanta looks well positioned to keep compounding.

6.3 GE Vernova (GEV):

A Great Way to Play the Grid Build-Out

GE Vernova stands out as one of the clearest public-market ways to gain exposure to the grid investment cycle. The company sits at the center of global power equipment and electrification, with a footprint that spans generation, grid hardware, software, and services. That breadth gives it exposure to several of the forces shaping the next phase of the electricity system, while its installed base creates a durable stream of higher-quality service revenue over time.

What makes the story especially compelling in the context of this report is the Electrification segment. This business includes grid solutions, power conversion and storage, and software used to support the network.

Grid solutions account for the largest share of that segment, which gives GE Vernova direct exposure to the upgrade cycle in transmission and distribution. As spending on substations, transformers, switchgear, HVDC links, and automation moves higher, GE Vernova is positioned to capture a meaningful share of that capital deployment.

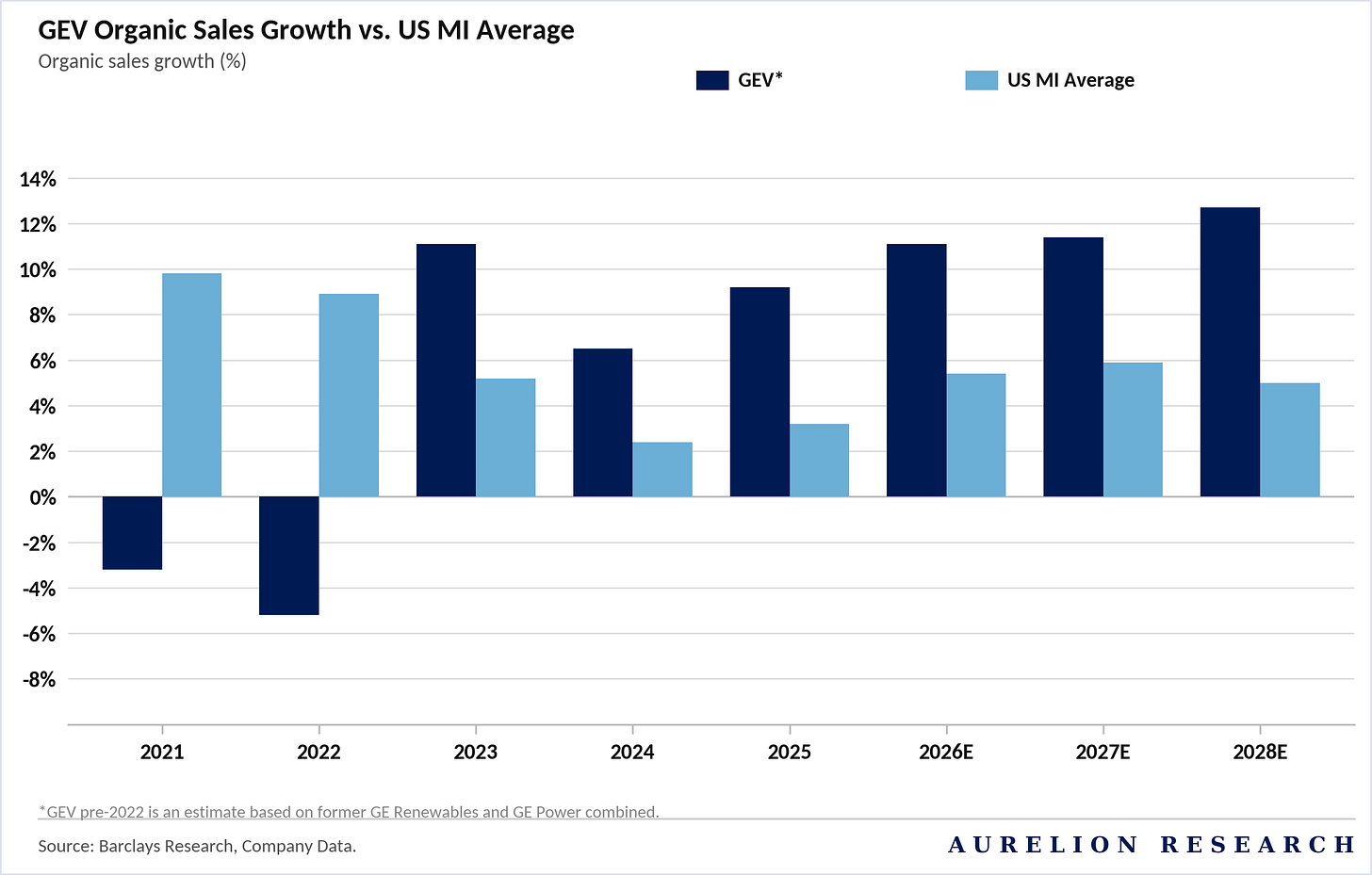

The broader setup also looks attractive. After a difficult period earlier in the decade, growth has inflected sharply. As the chart below shows, organic sales growth has moved ahead of the U.S. multi-industry average and is expected to stay there through 2028. That acceleration reflects improving demand across power and electrification, better execution, and a healthier order backdrop. It also supports the view that GEV is entering a period where stronger revenue growth can feed into much better earnings and cash generation.

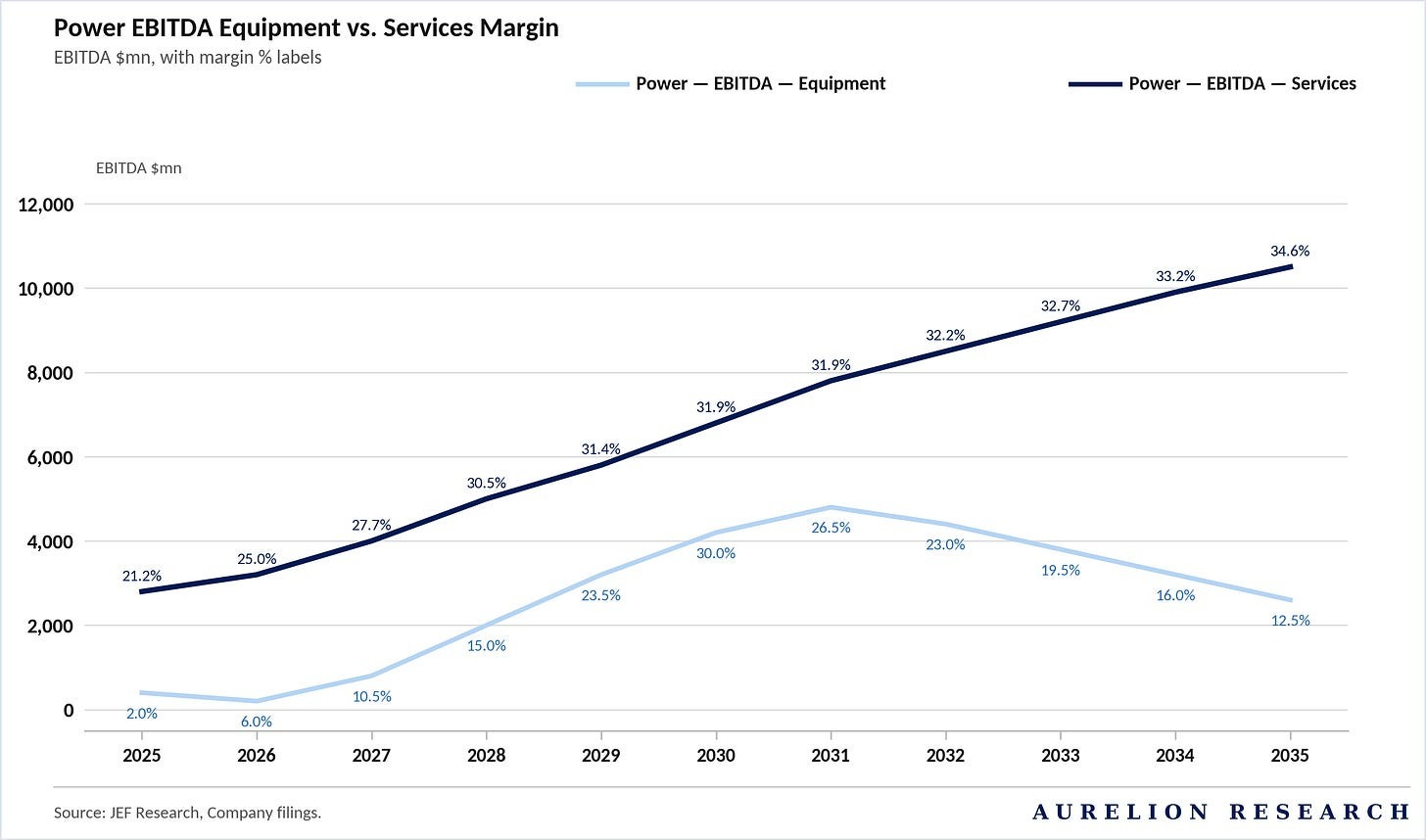

A key part of the thesis sits in the mix. The Power segment carries a large installed base, and service revenue attached to that fleet is far more attractive than equipment revenue. The margin chart makes that point clear.

Services are already highly profitable and continue to expand, while equipment margins recover from a lower base. As the revenue mix keeps shifting toward services and execution improves across the portfolio, group profitability has room to move materially higher over the next several years.

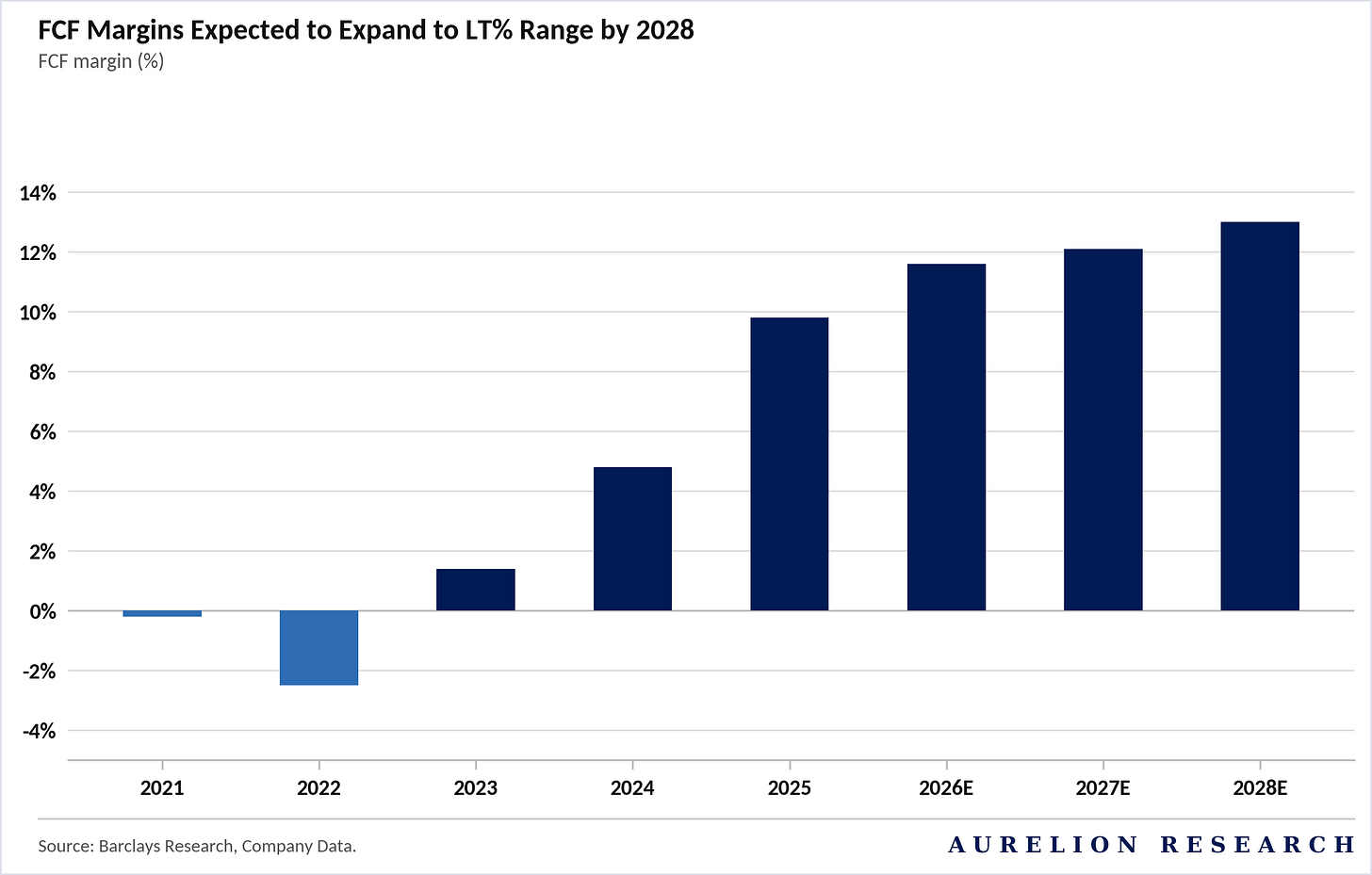

That operating improvement should show up very clearly in free cash flow. After moving through a lower-margin and more volatile phase, GEV is now reaching the point where higher earnings, better mix, and cleaner execution can translate into a much stronger cash profile. The FCF chart points to a business that could move into a low-teens margin range by 2028, which would represent a major step-up from recent history and place the company in a much stronger position from a capital allocation standpoint.

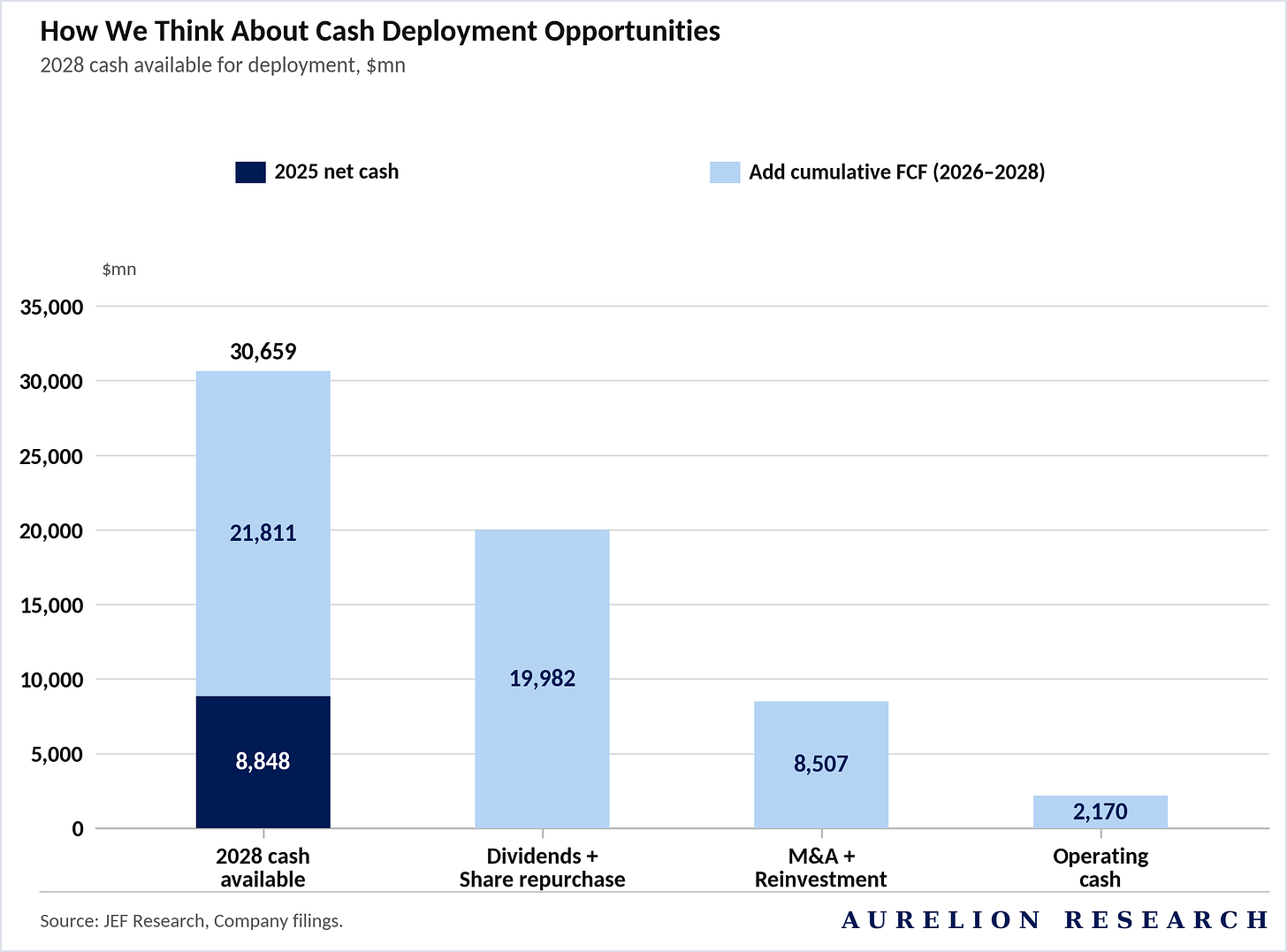

That cash generation opens another part of the upside. By 2028, the company could have a very large amount of cash available for deployment.

Management would then have meaningful room to balance shareholder returns, internal reinvestment, and external growth opportunities. In a market where grid and power assets remain strategically valuable, that flexibility could become an important advantage.

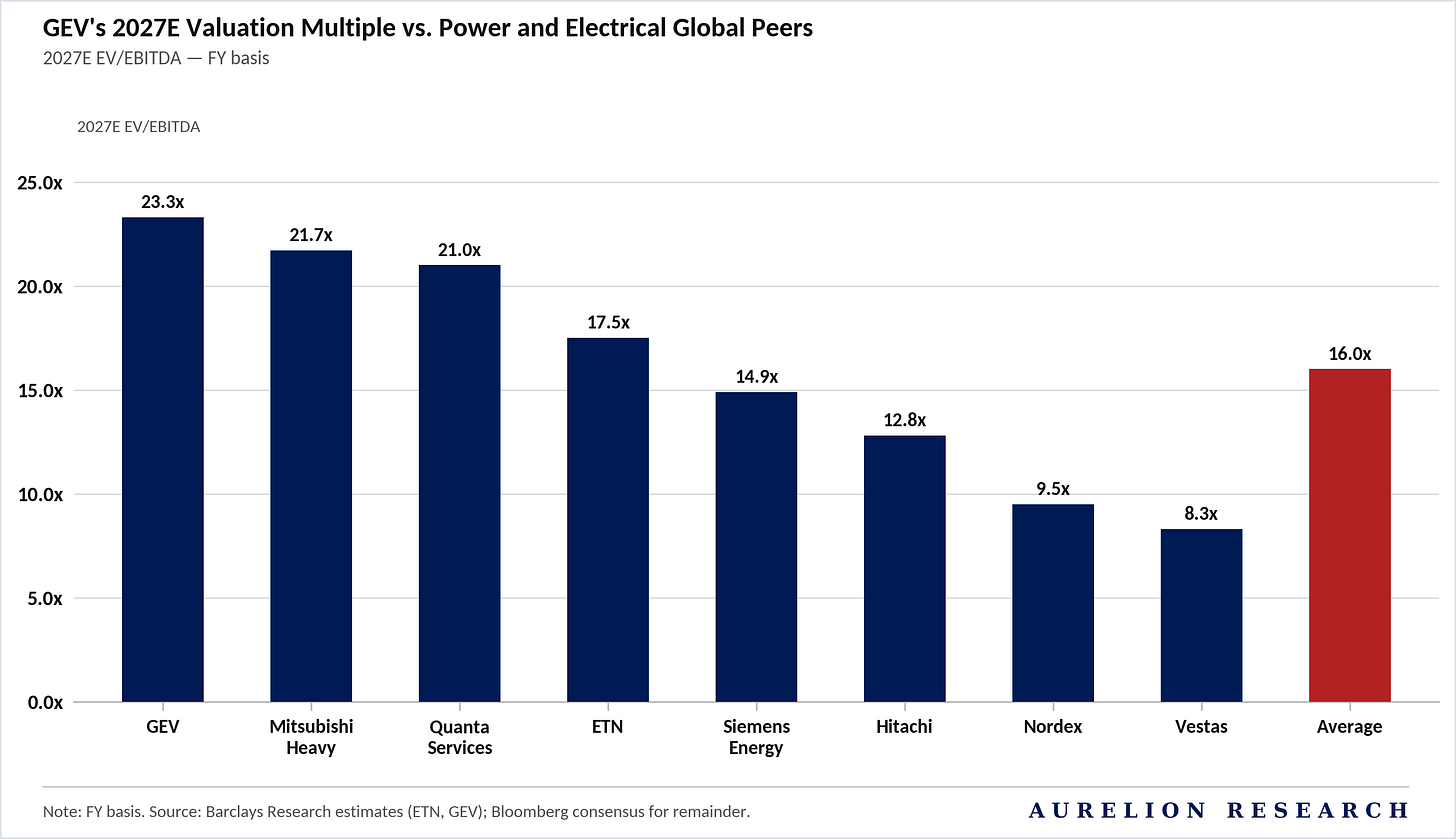

Valuation still looks reasonable when viewed against that runway. Even after the move in the stock, the multiple can be justified by the quality of the end markets, the scarcity value of the asset, and the earnings profile that can emerge as margins normalize and backlog converts.

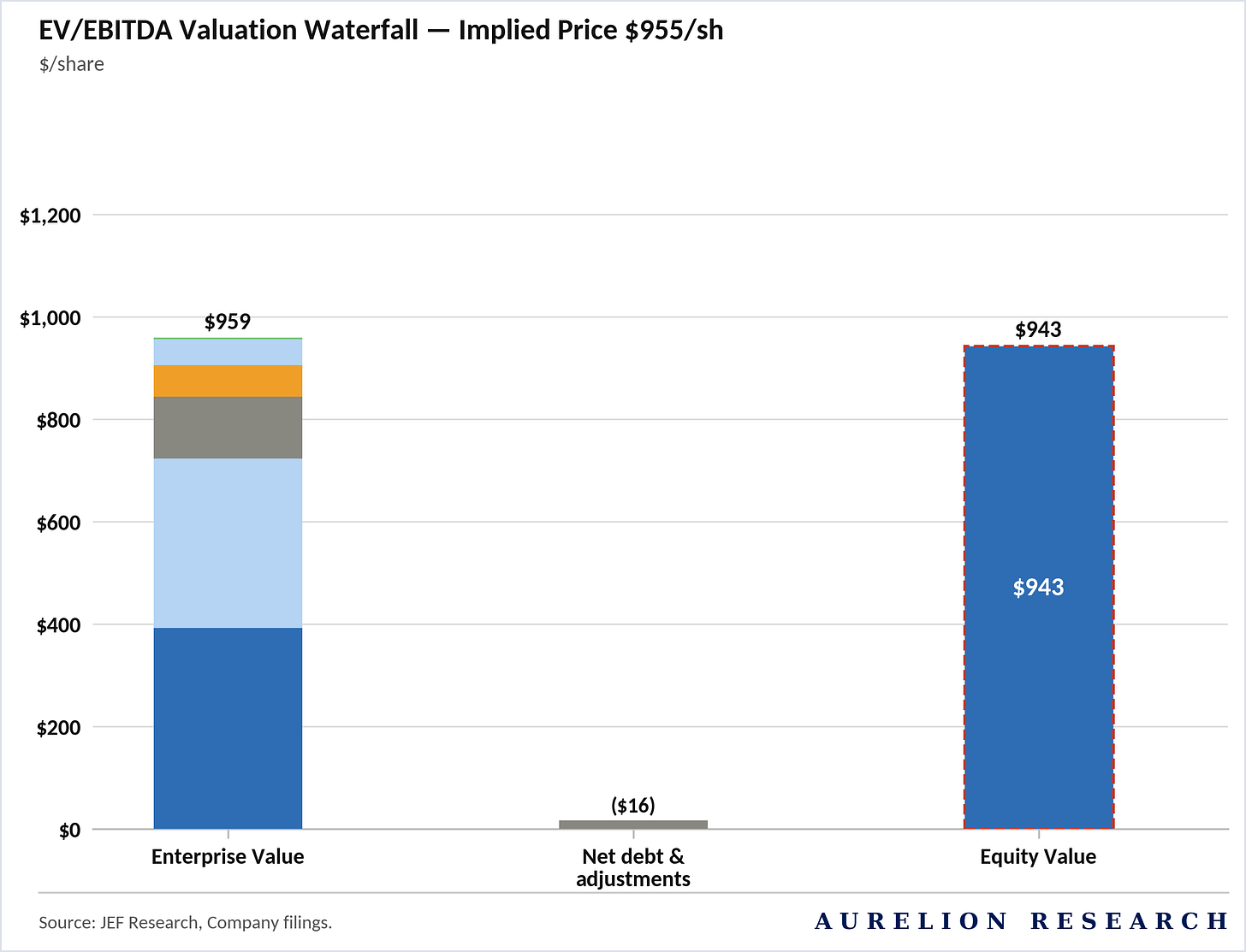

The valuation bridge shown below points to implied upside toward the mid-$900s per share, broadly in line with the upper-end analyst framework referenced in your notes. For a company with GE Vernova’s positioning, that still leaves room for appreciation if execution remains strong and electrification demand continues to build.

GE Vernova stands out here because it offers direct exposure to one of the most important themes in global power through a company with scale, a strong installed base, and real reach across the grid value chain. Its footprint spans transmission equipment, electrification, and the broader shift toward a more flexible and digital power system. If grid investment continues to move higher over the coming years, GE Vernova looks well placed to benefit.

We are aligned with Jefferies $1,030 upside scenario, which implies roughly 17.4% upside from a share price of $877. A stronger global need for compute capacity could push demand higher across both Power and Electrification, making them more meaningful contributors to 2028 EBITDA and supporting a higher valuation alongside upside to current estimates.

That upside view is based on a sum-of-the-parts EBITDA framework.

Like us, Jefferies sees meaningful room for margin expansion through the cycle, especially in gas OEM and services. The firm also expects peak orders to remain several years away, with continued margin improvement supporting further positive estimate revisions along the way.

GEV is not cheap, which explains why it is not our favorite name in the space. The stock already trades at a premium to the peer group average, and that is why the upside from here is closer to 17% than something more substantial.

7. Our Final Take on Grid Infrastructure

Everyone needs more electricity.

AI, data centers, electric vehicles, factories coming back onshore, buildings switching away from gas. All of it pulls in the same direction, and the grid carrying that power was built for a world that no longer exists.

That is what this thematic is really about. The physical infrastructure connecting generation to consumption has to grow, and the investment required to make that happen is already flowing. Utilities are committing capital at a pace not seen in a generation. Projects are breaking ground.

What makes this genuinely compelling is the breadth of ways to participate. Companies building the lines. Manufacturers supplying the hardware the new grid runs on. Engineers designing it before any physical work begins. Each benefits as the cycle deepens, each from a different angle.

We are early. The gap between where the grid sits today and where it needs to be is large enough that this spending cycle has years of runway ahead.

Daniel’s Deep Dive & The Aurelion Team

Reminder: Nothing you read here is financial advice. I am sharing my personal opinions and research, not telling you what to buy, sell, or hold. I am not a financial advisor, and this newsletter should never be seen as a recommendation to invest in any security.

| A guest post by

|

Very informative, great collab!

Masterclass.