Games Workshop: From Hobby Empire to Long-Term Compounder

In today’s analysis, we dive into the world of fantasy battles, loyal fans, and finely detailed miniatures. At first glance, it may not seem like the foundation for a high-quality investment — but the numbers tell a different story. What if behind the hobby lies one of the most quietly impressive businesses in the market?

What Does Games Workshop Actually Do?

Games Workshop is a British company headquartered in Nottingham, best known for its iconic tabletop franchises, particularly Warhammer 40,000 and Warhammer Age of Sigmar. At the heart of its business model lies the Warhammer universe — an expansive intellectual property that spans lore, miniatures, board games, merchandise, and digital adaptations. The company develops, manufactures, and sells miniature-based tabletop games set in richly imagined fantasy and science fiction worlds. Every product it offers ties back to these original settings, giving GW full control over its creative and commercial ecosystem. Over the years, the company has cultivated a deeply loyal and enthusiastic global fanbase around this universe. But let’s take a closer look at the details of how Games Workshop generates its revenue.

In its annual report, Games Workshop (referred to as GW from here on) outlines several revenue-generating segments.

The Trade segment includes revenue through independent retailers, both physical locations and their online stores, as well as revenue from the company’s own publishing division, Black Library. So, for example, if a hobby store or a website like amazon.com offers GW products, that revenue is included in this segment. In 2024, this segment comprised approximately 7,200 stores across 73 countries and accounted for around 58% of total revenue.

The Retail segment consists of revenue made through GW’s own stores. As of 2024, the company operated 548 locations in 23 countries, contributing roughly 24% of overall revenue. These stores not only function as retail outlets but also serve as gathering places for the community, where hobbyists can paint, collect, and engage in battles. They are a key driver of customer loyalty.

Online revenue stems from sales made through GW’s own web store, which represented about 18% of total revenue in 2024. This segment is still relatively small, as GW relied heavily on independent online retailers for many years and only began expanding its own web store more actively in recent years.

Outside of its core operating business, GW also reports a separate segment for licensing. Licensing revenue comes primarily from agreements with third-party developers who create video games based on the Warhammer universe. While this segment contributes only a relatively modest portion of overall revenue, it represents a growing opportunity and helps expand the reach of the Warhammer brand beyond the tabletop space. It is a high-margin segment, but one with highly volatile revenues, as the release of new games follows a strongly cyclical business model. We will take a closer look at this later on.

The company’s strategic focus lies squarely on the development and distribution of its tabletop games. According to management, the priority is long-term success rather than chasing strong short-term KPIs. This long-term mindset has enabled GW to build a loyal global fanbase, establish a distinct and resilient brand identity, and maintain tight control over both production and marketing. Over time, this has allowed the company to carve out a unique niche within the gaming and collectibles market.

Now that we understand what GW actually does, it’s time to take a closer look at the company’s growth.

Where Does the Growth Come From?

In 2015, Kevin Rountree stepped into the role of CEO at Games Workshop. At the time, the company was facing serious challenges. It had fallen behind in digitalization, community engagement had dropped to a minimum, and the prices of its miniatures had reached levels that turned away parts of its customer base. As a result, GW began losing both customers and market share to smaller, more agile competitors.

When Rountree took over, he introduced a new strategic direction beginning in 2016. This included a stronger presence on digital platforms, renewed efforts to engage the community — notably through organized events — as well as initiatives to lower the barrier to entry for new players. He also pushed for collaborations in video gaming and streaming, helping to expand the reach of the Warhammer universe.

These changes marked a turning point. For the first time in years, Games Workshop returned to growth.

Let’s leave the past behind and look at the current landscape. In 2023, the global market for tabletop games was valued at approximately USD 27.27 billion. By 2029, it is expected to grow to USD 49.17 billion, reflecting a solid annual growth rate of 10.32%. The core audience for miniature-based games likely includes around 5 million active players. On top of that, there is an additional pool of 10 to 15 million potential customers who are interested in fantasy video games and books.

What gives Games Workshop a unique advantage is that it has already built a vast and detailed universe of characters, games, and stories — and, just as importantly, a large and passionate community of collectors and players ready to engage with it.

Games Workshop is following a clear and focused strategy to drive growth. The company emphasizes organic expansion and has consistently ruled out acquisitions as a growth avenue. Instead, it aims to grow its customer base within existing core markets like Europe and North America, while also pushing into new geographic regions. One of the most promising opportunities lies in Asia, where the company still sees significant untapped potential.

Over the past five years, Games Workshop has delivered impressive organic growth. Sales have increased by an average of 13% per year, while profits have grown at an annual rate of 18%. However, this growth is not entirely steady. It is subject to cycles, as the release of new products in existing markets plays a central role. The typical product cycle lasts between three and five years.

A major source of growth in existing markets has been the successful acquisition of new customers. One of the core problems identified by management was the steep entry barrier for beginners. Building and painting an army took too much time and was too expensive, which discouraged many potential newcomers. In response, the company introduced more affordable starter sets, simplified the painting process and made the game rules more accessible. These changes reduced the time it takes for new players to get started and led to faster engagement with the hobby.

Looking ahead, management is aiming for continued double-digit growth over the medium to long term. The company plans to open more stores in Europe and North America. In the longer term, it sees significant potential in expanding across Latin America and East Asia.

In addition to attracting new customers, existing players also contribute meaningfully to revenue over time. Many of them continue to invest in new armies, often over several years. GW takes advantage of this by launching a new edition every three years. Each cycle brings new rulebooks, miniatures, paints and related content. Between editions, individual product releases help maintain momentum and engagement.

Pricing power is another important driver of growth. Games Workshop has been able to increase prices on a regular basis without losing customer loyalty. These price increases have played a major role in boosting profit growth.

Given the broader market growth of just over ten percent, the company’s ongoing expansion into new regions and its ability to win new customers in established markets, it is reasonable to expect that GW can continue to grow revenue at a rate of around 14% per year. The only real drawback is that a large portion of the profit is consistently paid out as dividends. While this is attractive for shareholders in the short term, it may limit the company’s long-term potential. That capital could arguably be used more effectively by accelerating expansion efforts, particularly in the highly promising Asian market.

What I personally find especially compelling is that management remains fully focused on the core business — the development, production, and distribution of miniatures — while deliberately outsourcing everything outside that expertise through licensing partnerships.

One of these partnerships was with the game publisher Focus Entertainment, which developed Space Marine 2 based on the Warhammer 40,000 universe under a licensing agreement with GW. The game has since become a major hit, attracting over 4.5 million players and significantly expanding the reach of the Warhammer brand. It was such a success that the development of a sequel has already been announced. While licensing revenue from video games tends to be cyclical and will likely decline in periods between major releases, the impact of Space Marine 2 goes far beyond short-term income. Most importantly, the game has introduced a large number of new players to the Warhammer universe and could lead to lasting growth in the company’s core tabletop business. This partnership contributed to a roughly 33 percent increase in earnings per share during the second half of 2024. However, this figure should be interpreted with caution, as a significant part of the increase was driven by cyclical licensing income.

Another long-term partnership was established with Amazon. On December 10, 2024, Games Workshop announced a long-awaited deal with the streaming giant, granting Amazon exclusive rights to develop and distribute films and series set in the Warhammer 40,000 universe. After years of negotiation, the agreement is now finalized. Production of the first Amazon-exclusive series is expected to begin soon, although a release is still several years away.

While the deal will have no immediate financial impact, it could prove to be a defining moment for the company’s long-term trajectory. For the first time, Warhammer will reach mainstream audiences on a global streaming platform — a move that could dramatically boost brand visibility, drive new players toward the tabletop hobby, and generate substantial future licensing revenue.

In summary, management remains focused on long-term organic growth, and an annual growth rate of 14 percent appears realistic in the short to medium term. In addition, strategic partnerships offer significant potential to accelerate that growth even further in the years ahead.

How GW Stays Ahead of the Game

Since its founding, Games Workshop has steadily carved out a unique position in a niche market. This standing is built on several strategic pillars that together form the company’s moat. At the core of its competitive edge are a powerful intellectual property, a broad network of company-owned stores, and a global, highly engaged community of gamers and collectors. The company maintains full control over the entire value chain, from design and production to distribution. This structure ensures both flexibility and speed, which are critical in a niche industry.

One frequently discussed risk is the rise of 3D printing. In theory, it could allow users to reproduce GW’s miniatures at a fraction of the cost. But in practice, the Warhammer community places immense value on authenticity and quality. The original miniatures are not just gaming pieces. They are collector’s items. Within the scene, ownership of official figures carries real significance. Participation in tournaments and community events is typically restricted to players using the genuine product. This reinforces the cultural and emotional value of buying from Games Workshop.

There’s also a deeper psychological factor at play. These miniatures satisfy a collector’s instinct that knockoffs simply can’t replicate. It’s similar to stamp collecting. With the right printer and paper, a rare stamp could be duplicated in high detail. But that would defeat the purpose. The value lies in authenticity. Warhammer players are no different. Their competitive drive and desire to belong to the community are tightly linked to owning original pieces. For this reason, 3D printing does not pose a meaningful threat to GW’s business model.

The broader tabletop market is filled with smaller competitors. Very few of them offer the same depth of lore, the wide variety of products, the steady stream of new releases, the retail and partner network, or the strength of the Warhammer community. What sets GW apart is not only its expansive universe but also the loyalty of its fanbase. It’s this long-standing community that gives the company its staying power. Participation in official tournaments and the sense of being part of something larger builds customer loyalty in a way that newcomers struggle to replicate. This effect is comparable to the dynamics of a social network. Large platforms continue to grow because of their user base, while smaller ones often struggle to gain traction or scale. The same principle applies to the Warhammer ecosystem and its immense reach.

In short, Games Workshop has positioned itself as the clear leader in a highly fragmented niche. Its competitive moat is built around intellectual property, product breadth, global infrastructure, brand strength, and community loyalty. This foundation gives GW a durable edge and reinforces its leadership in the world of tabletop gaming.

Is Selling Miniatures Really That Profitable?

Thanks to its strong market position, significant pricing power, and tight cost control through ownership of its own production and logistics infrastructure, Games Workshop operates with remarkably high profitability.

This is clearly reflected in its gross profit margin, which has remained high and relatively stable over time.

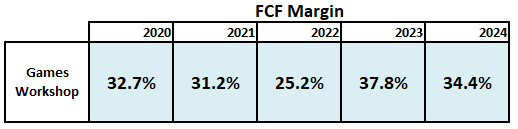

In the 2024 financial year (June 1, 2023 to May 31, 2024), GW allocated around 6.5 percent of its revenue to capital expenditures, mainly to expand production capacity with the construction of a fourth factory. Despite these investments, the company’s free cash flow (FCF) margin remained stable, which shows that Games Workshop is a "cash machine" that regularly generates high FCF.

However, it’s worth noting that the company’s pricing power should not be pushed too far. Many players are already voicing concerns that the cost of miniatures is becoming too high. A dissatisfied community could eventually pose a threat to the business model. There is therefore a risk that profitability could come under pressure if input or labor costs rise significantly.

I could go on listing strong profitability metrics, but the point should be clear by now: Games Workshop is a highly profitable company.

A quick look at the balance sheet adds to this picture. GW currently has negative net debt, meaning that its cash and cash equivalents exceed its total liabilities. This provides financial flexibility, whether for future expansion or to survive difficult market conditions.

Does GW Also Pay A Dividend?

Let's first take a look together at what GW's dividend strategy is:

We will only pay dividends out of cash which is truly surplus to the business, after making allowance for the costs of new retail store openings, regular capital expenditure and maintenance, investment in tooling, plus a sum to ensure the business has sufficient working capital for its needs. - Games Workshop Investor Relations

I already hinted my somewhat critical opinion regarding GW's dividend policy in the growth chapter. Games Workshop has a generous dividend policy and regularly distributes up to 80% of its free cash flow to shareholders. In my view, this capital could be used more efficiently in the expansion of the company.

However, dividend-focused investors in particular should not be tempted by the relatively high dividend yield, as the increase and regular payment of dividends is not GW's top priority and dividend payments have already stagnated or been reduced in recent years.

What Does The Valuation Look Like?

I valued GW with the help of a DCF model. In doing so, I have conservatively assumed that the company will grow by 10–14% in the coming years. This lies between GW's average growth over the last five years and the forecast market growth for table-top games. This conservative assumption excludes growth from licensing or special effects such as the Amazon series, and therefore provides a certain margin of safety. Furthermore, I have assumed an FCF margin of 30% for the coming years, which is slightly below the average (32%) of the last five years. Finally, according to Damodaran, I have made assumptions about the WACC (8%), the risk-free rate (3.88%), the beta (0.9) and the equity risk premium (4.6%). I arrive at a fair value of £168. GW is currently trading at around £151. However, any investment should include a margin of safety to allow for a price discount and to provide a buffer against unexpected developments. After applying a 30% margin of safety, my target entry price comes to £117. So, in my view, GW is currently overvalued by around 29%.

Let's Conclude!

A look back at the analysis reveals that GW is a company of outstanding quality. It has a long-term and strong moat and is the market leader in a niche area. The company's competitive advantage enables it to achieve very high profitability with solid growth rates and a high free cash flow. In addition, the company is essentially debt-free. In my view, this company is a compounder that is able to provide its investors with above-average returns over a long period of time. An entry does not appear attractive at the current price, but it could quickly become appealing in the event of a correction.

I hope you enjoyed the analysis and I’d love to hear your feedback. Subscribe to get future updates on Games Workshop and never miss out on compelling investment ideas.